Fill Out Your IRS Schedule C 1040 Template

Fill Out Your IRS Schedule C 1040 Template

Navigating the world of taxes can be daunting, especially for those who run their own business or work as freelancers. For individuals in these categories, the IRS Schedule C 1040 form becomes an essential part of their tax filing process. This form is designed to report income or loss from a business you operated or a profession you practiced as a sole proprietor. At its core, Schedule C provides a way to calculate the profit or loss from your business activities by allowing you to delineate your business income, cost of goods sold, and various expenses. This calculation not only determines the amount of tax you owe but also impacts your self-employment tax and net earnings. Properly reporting on Schedule C can unlock potential tax savings, as it offers the opportunity to deduct legitimate business expenses, ranging from advertising to utilities, which reduces your taxable income. Nonetheless, filling out Schedule C accurately requires a meticulous examination of your business finances and can significantly influence your overall tax liability, highlighting the importance of understanding each part of the form to ensure compliance and optimize your tax situation.

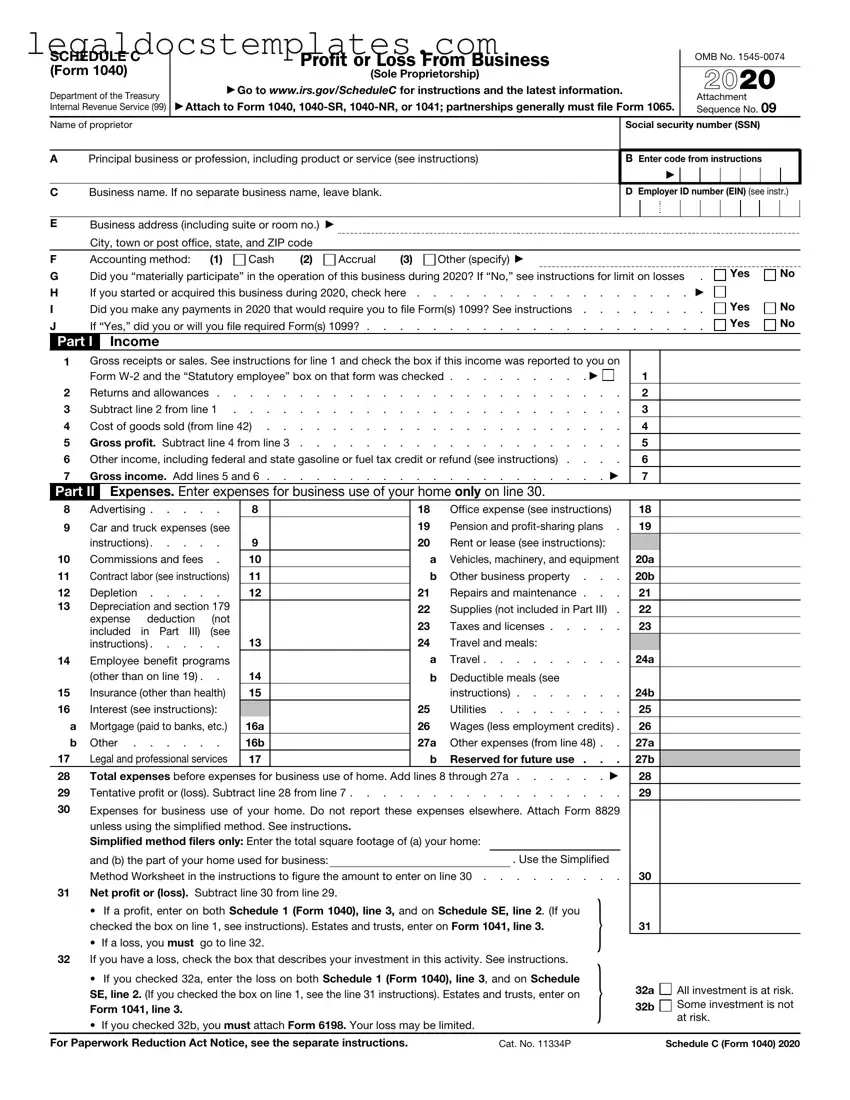

SCHEDULE C |

|

Profit or Loss From Business |

|

OMB No. |

|||||||

|

|

||||||||||

(Form 1040) |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||

|

(Sole Proprietorship) |

|

2020 |

|

|||||||

Department of the Treasury |

|

▶ Go to www.irs.gov/ScheduleC for instructions and the latest information. |

|

|

|||||||

|

|

|

|

Attachment |

|||||||

Internal Revenue Service (99) |

|

▶ Attach to Form 1040, |

Sequence No. 09 |

||||||||

Name of proprietor |

|

|

|

Social security number (SSN) |

|||||||

|

|

|

|

|

|

|

|

|

|

||

A |

Principal business or profession, including product or service (see instructions) |

|

B Enter code from instructions |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

▶ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

C |

Business name. If no separate business name, leave blank. |

D Employer ID number (EIN) (see instr.) |

|||||||||

EBusiness address (including suite or room no.) ▶ City, town or post office, state, and ZIP code

F |

Accounting method: |

(1) |

Cash |

(2) |

Accrual |

(3) |

Other (specify) ▶ |

G |

Did you “materially participate” in the operation of this business during 2020? If “No,” see instructions for limit on losses . |

||||||

H |

If you started or acquired this business during 2020, check here . |

. . . . . . . . . . . . . . . . ▶ |

|||||

I |

Did you make any payments in 2020 that would require you to file Form(s) 1099? See instructions |

||||||

J |

If “Yes,” did you or will you file required Form(s) 1099? |

||||||

Yes

Yes  No

No

Yes

Yes

No

No

Yes

Yes  No

No

Part I Income

1 |

Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on |

|

|

|||||||||||

|

Form |

. . . . . . . . |

. ▶ |

1 |

|

|||||||||

2 |

Returns and allowances |

. . . . . . . . . . . |

|

2 |

|

|||||||||

3 |

Subtract line 2 from line 1 |

. . . . . . . . . . . |

|

3 |

|

|||||||||

4 |

Cost of goods sold (from line 42) |

. . . . . . . . . . . |

|

4 |

|

|||||||||

5 |

Gross profit. Subtract line 4 from line 3 |

. . . . . . . . . . . |

|

5 |

|

|||||||||

6 |

Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . |

6 |

|

|||||||||||

7 |

Gross income. Add lines 5 and 6 |

. . . . . . . . |

. |

. ▶ |

7 |

|

||||||||

Part II |

Expenses. Enter expenses for business use of your home only on line 30. |

|

|

|

|

|

||||||||

8 |

Advertising |

8 |

|

|

18 |

Office expense (see instructions) |

18 |

|

||||||

9 |

Car and truck expenses (see |

|

|

|

19 |

Pension and |

19 |

|

||||||

|

instructions) |

9 |

|

|

20 |

Rent or lease (see instructions): |

|

|

||||||

10 |

Commissions and fees . |

10 |

|

|

a |

Vehicles, machinery, and equipment |

20a |

|

||||||

11 |

Contract labor (see instructions) |

11 |

|

|

b |

Other business property . . . |

20b |

|

||||||

12 |

Depletion |

12 |

|

|

21 |

Repairs and maintenance . . . |

21 |

|

||||||

13 |

Depreciation and section 179 |

|

|

|

22 |

Supplies (not included in Part III) . |

22 |

|

||||||

|

expense deduction (not |

|

|

|

|

|||||||||

|

|

|

|

23 |

Taxes and licenses |

23 |

|

|||||||

|

included in Part III) (see |

|

|

|

|

|||||||||

|

instructions) |

13 |

|

|

24 |

Travel and meals: |

|

|

|

|

|

|||

14 |

Employee benefit programs |

|

|

|

a |

Travel |

24a |

|

||||||

|

(other than on line 19) . . |

14 |

|

|

b |

Deductible meals (see |

|

|

|

|

|

|||

15 |

Insurance (other than health) |

15 |

|

|

|

instructions) |

24b |

|

||||||

16 |

Interest (see instructions): |

|

|

|

25 |

Utilities |

25 |

|

||||||

a |

Mortgage (paid to banks, etc.) |

16a |

|

|

26 |

Wages (less employment credits) . |

26 |

|

||||||

b |

Other |

16b |

|

|

27a |

Other expenses (from line 48) . . |

27a |

|

||||||

17 |

Legal and professional services |

17 |

|

|

b |

Reserved for future use . . . |

27b |

|

||||||

28 |

Total expenses before expenses for business use of home. Add lines 8 through 27a . . . . |

. |

. ▶ |

28 |

|

|||||||||

29 |

Tentative profit or (loss). Subtract line 28 from line 7 |

. . . . . . . . . . . |

|

29 |

|

|||||||||

30 |

Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 |

|

|

|||||||||||

|

unless using the simplified method. See instructions. |

|

|

|

|

|

|

|

|

|

||||

|

Simplified method filers only: Enter the total square footage of (a) your home: |

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|||||

|

and (b) the part of your home used for business: |

|

|

|

|

. Use the Simplified |

|

|

||||||

|

Method Worksheet in the instructions to figure the amount to enter on line 30 |

30 |

|

|||||||||||

31 |

Net profit or (loss). Subtract line 30 from line 29. |

|

|

|

|

|

} |

|

|

|

||||

|

• If a profit, enter on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you |

|

|

|

|

|||||||||

|

checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. |

|

|

31 |

|

|||||||||

|

• If a loss, you must go to line 32. |

|

|

|

|

|

|

|

|

|||||

32 |

If you have a loss, check the box that describes your investment in this activity. See instructions. |

|

} |

|

|

|

||||||||

|

• If you checked 32a, enter the loss on both Schedule 1 (Form 1040), line 3, and on Schedule |

|

|

32a |

All investment is at risk. |

|||||||||

|

SE, line 2. (If you checked the box on line 1, see the line 31 instructions). Estates and trusts, enter on |

|

|

|||||||||||

|

|

|

32b |

Some investment is not |

||||||||||

|

Form 1041, line 3. |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

at risk. |

|||

|

• If you checked 32b, you must attach Form 6198. Your loss may be limited. |

|

|

|

|

|

||||||||

For Paperwork Reduction Act Notice, see the separate instructions. |

|

|

Cat. No. 11334P |

|

|

|

|

Schedule C (Form 1040) 2020 |

||||||

Schedule C (Form 1040) 2020 |

Page 2 |

|

Part III |

Cost of Goods Sold (see instructions) |

|

33 |

Method(s) used to |

|

|

|

|

|

|

|

value closing inventory: |

a |

Cost |

b |

Lower of cost or market |

c |

Other (attach explanation) |

34Was there any change in determining quantities, costs, or valuations between opening and closing inventory?

If “Yes,” attach explanation |

Yes |

No

35 |

Inventory at beginning of year. If different from last year’s closing inventory, attach explanation . . . |

35 |

|

|||

36 |

Purchases less cost of items withdrawn for personal use |

36 |

|

|||

37 |

Cost of labor. Do not include any amounts paid to yourself |

37 |

|

|||

38 |

Materials and supplies |

38 |

|

|||

39 |

Other costs |

39 |

|

|||

40 |

Add lines 35 through 39 |

40 |

|

|||

41 |

Inventory at end of year |

41 |

|

|||

42 |

Cost of goods sold. Subtract line 41 from line 40. Enter the result here and on line 4 |

42 |

|

|||

Part IV |

Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 |

|||||

|

|

and are not required to file Form 4562 for this business. See the instructions for line 13 to find out if you must |

||||

|

|

file Form 4562. |

|

|

|

|

43 |

When did you place your vehicle in service for business purposes? (month/day/year) |

▶ |

/ |

/ |

|

|

44Of the total number of miles you drove your vehicle during 2020, enter the number of miles you used your vehicle for:

a |

Business |

b Commuting (see instructions) |

c Other |

|

45 |

Was your vehicle available for personal use during |

. . . . . . . . . . . . . |

Yes |

|

46 |

Do you (or your spouse) have another vehicle available for personal use?. |

. . . . . . . . . . . . . |

Yes |

|

47a |

Do you have evidence to support your deduction? |

. . . . . . . . . . . . . |

Yes |

|

b |

If “Yes,” is the evidence written? |

. . . . . . . . . . . . . |

Yes |

|

Part V Other Expenses. List below business expenses not included on lines

No

No

No

No

No

No

48 Total other expenses. Enter here and on line 27a . . . . . . . . . . . . . . . .

48

Schedule C (Form 1040) 2020

| Fact Name | Description |

|---|---|

| Purpose of Form | The IRS Schedule C 1040 form is used by sole proprietors to report income or loss from a business they operated or a profession they practiced as a sole proprietor. |

| Attachment to Form 1040 | This form is a part of the Form 1040, the U.S. individual income tax return, and is filed alongside it. |

| Information Required | The form requires information about the business’s profit and loss, including income, expenses, and the cost of goods sold. |

| Self-Employment Tax Calculation | Income shown on Schedule C is used to determine the amount of Self-Employment Tax owed by the proprietor, calculated on Schedule SE. |

| Use for Small Businesses | It's most commonly used by individuals operating as sole proprietors, including freelancers and independent contractors, to report their business income. |

| Governing Law | The form is governed by the Internal Revenue Code, which is federal law applicable across all states. There are no state-specific governing laws for Schedule C. |

The IRS Schedule C 1040 form is a crucial document for individuals who operate as sole proprietors. This form is designed to report income or loss from a business you operated or a profession you practiced as a sole proprietor. Accurately filling out this form is essential for tax reporting purposes and to ensure compliance with IRS regulations. Below are step-by-step instructions to guide you through the process of filling out the Schedule C form. It is recommended to have all pertinent financial records available before beginning this process to ensure accuracy and completeness of the information reported.

After completing the Schedule C form, attach it to your Form 1040 or 1040-SR and submit it to the IRS by the tax filing deadline. Retain a copy of the form and all supporting documents for your records. Filling out Schedule C accurately and comprehensively enables you to correctly report your business income and expenses, which can help maximize your eligible deductions and minimize the risk of IRS audits.

The IRS Schedule C 1040 form is a document that individuals who are self-employed, either as a sole proprietor or as an independent contractor, use during tax filing time. This form is utilized to report income or loss from a business operation or profession conducted as a single person. Essentially, it calculates the gross income, expenses, and potential deductions associated with running a business, helping to determine the net profit or loss. This net amount is then transferred to the individual's personal income tax return, impacting the overall tax liability or refund.

Filing a Schedule C 1040 form is required for any individual who operates a business on their own, including a sole proprietorship or freelance work, and has earned income that needs to be reported to the Internal Revenue Service (IRS). There are several criteria that typically require the filing of Schedule C, including:

It’s important for individuals in these situations to maintain accurate records of their business transactions throughout the fiscal year to ensure the completeness and accuracy of the Schedule C form.

To accurately fill out the Schedule C 1040 form, several pieces of information about your business will be required, including:

Organized records and receipts will simplify the process of completing the Schedule C form and help to ensure that all eligible deductions are claimed, potentially reducing your taxable income.

Filing a Schedule C 1040 form directly impacts your personal income taxes by adding the net profit or loss from your business to your total taxable income. The net profit from your business operations—calculated as your total income minus your deductible expenses—contributes to your overall adjusted gross income. This can affect your tax bracket and eligibility for certain tax credits and deductions, leading to:

Additionally, self-employed individuals filing Schedule C may be responsible for paying self-employment tax, which covers Social Security and Medicare contributions. Hence, the outcome of filing a Schedule C can significantly affect both the amount of taxes owed and the individual's eligibility for social benefits.

Filing taxes can often feel like navigating through a maze, especially when dealing with the IRS Schedule C form of the 1040, which is used by sole proprietors. A common mistake many make is not accurately reporting all their income. This doesn't just mean the money made from direct sales but also includes any other forms of income, such as interest on business accounts or any other payments received. It's easy to overlook these, but they are essential for a complete and accurate filing.

Expenses can also pose a significant hurdle. Often, individuals either overestimate or underestimate their deductible expenses. It's crucial to keep diligent records throughout the year to ensure that all legitimate business expenses are captured and properly documented. This includes keeping receipts and noting the business purpose of each expense. Accurate tracking helps avoid the mistake of missing out on valuable deductions or claiming inappropriate ones.

Another area where errors frequently occur is in the calculation of the home office deduction. Those working from home must meet specific criteria to claim this deduction, and the space must be used regularly and exclusively for business. Some mistakenly believe any use of a home office qualifies, not adhering to the strict requirements set by the IRS, potentially leading to issues upon review.

The use of incorrect forms is yet another mistake. The Schedule C is specifically for sole proprietors and single-member LLCs. However, owners of other types of businesses sometimes mistakenly use this form when other forms would be more appropriate for their business structure. Understanding the legal structure of your business and corresponding tax obligations is vital for proper filing.

Errors in reporting car and truck expenses also trip up many filers. For these expenses, one can opt to use either the standard mileage rate or actual expense method. However, switching between methods or inaccurately calculating expenses can lead to problems. Keeping a detailed mileage log and all receipts related to vehicle expenses is a good practice.

Miscategorizing employees as independent contractors or vice versa can lead to significant issues with the IRS. This not only affects how you report on Schedule C but also impacts employment taxes. Clear understanding of the distinction between an employee and an independent contractor based on IRS guidelines is essential.

Not correctly separating personal and business expenses is a frequent oversight. Even if you use your personal vehicle or home for business, you need to distinguish between its business and personal use strictly. This separation is crucial for accurate tax reporting and compliance with IRS rules.

Failing to report carryover losses is another area that is often neglected. If your business expenses exceed your income, you may have a net loss that can be carried over to the next tax year. However, not properly documenting or forgetting to report these losses can result in missing out on potential tax benefits.

Trying to deduct non-deductible expenses can also lead to complications. While many expenses are deductible, some, such as personal living expenses or fines and penalties, are not. Distinguishing between these is fundamental to avoiding claims that may be disallowed upon an audit.

Lastly, doing it all yourself without seeking professional guidance can be a mistake. Tax laws are complex and constantly changing. Professional tax advisors or accountants can provide valuable assistance in navigating these complexities, ensuring compliance, and potentially saving money.

When individuals engage in self-employment or operate a sole proprietorship, they often find themselves navigating the complexities of tax preparation with more than just the basic forms. An essential document for reporting profit or loss from a business is the IRS Schedule C (Form 1040). However, to provide a complete and accurate financial picture, several other forms and documents are frequently used in conjunction with Schedule C. These play a crucial role in ensuring that taxpayers meet their legal obligations while also maximizing potential deductions and credits.

While the IRS Schedule C (Form 1040) is central for those with self-employment income, understanding and utilizing these additional forms can be instrumental in navigating tax responsibilities effectively. It’s advisable for taxpayers to familiarize themselves with these documents or seek professional assistance to ensure accuracy and compliance, as well as to take full advantage of any deductions and credits for which they may be eligible. Navigating tax filings can be complex, but thorough preparation can significantly impact one’s financial health.

The IRS Form 1040, Schedule SE, is akin to Schedule C in its function to calculate taxes related to self-employment income. While Schedule C is used to report income or loss from a business you operated or a profession you practiced as a sole proprietor, Schedule SE is employed to figure the tax due on net earnings from self-employment. This connection is crucial as the income reported on Schedule C forms the basis for the self-employment tax calculated on Schedule SE. Both forms work in tandem to ensure self-employed individuals correctly report their business income and calculate the taxes owed for Social Security and Medicare.

Form 8829, Expenses for Business Use of Your Home, serves a complementary role to Schedule C for those who use part of their home for business. This form allows individuals to calculate and deduct the expenses of their home office, an essential tool for many small business owners and sole proprietors who operate from home. By delineating the proportion of the home used for business, Form 8829 directly affects the net profit or loss figure on Schedule C, impacting the overall taxable income reported to the IRS. This synergy ensures that entrepreneurs receive rightful deductions, thereby potentially lowering their taxable income.

The IRS Form 1040-ES, Estimated Tax for Individuals, aligns with Schedule C regarding the payment of taxes throughout the year. Sole proprietors, freelancers, and independent contractors use Schedule C to report their annual income or loss from a business. Based on this reported figure, Form 1040-ES is then used to calculate and pay estimated taxes quarterly. This pre-payment system helps individuals avoid underpayment penalties at year-end by spreading tax payments over the course of the year, reflecting the fluctuating income streams that are common among those who are self-employed.

Lastly, Form 1099-MISC (Miscellaneous Income) and its more recent version, Form 1099-NEC (Nonemployee Compensation), share a complementary relationship with Schedule C. These forms are used by businesses to report payments made to non-employees, such as independent contractors. For the recipients of these forms, the income reported on 1099-MISC or 1099-NEC must be reported on Schedule C if it pertains to their business operations. This requirement ensures that all income received for services rendered is accurately reported to the IRS. Notably, these forms are a key part of the documentation for both the payer and recipient, ensuring transparency and compliance with tax regulations.

Filling out the IRS Schedule C 1040 form, a crucial component of an individual's tax filing process, particularly for those who operate as sole proprietors or as single-member LLCs, needs careful attention. The form allows taxpayers to report income or loss from a business they operated or a profession they practiced as a sole proprietor. To ensure accuracy and compliance with tax laws, here are nine do's and don'ts to keep in mind:

Approaching the IRS Schedule C 1040 form with diligence and care can save taxpayers from future headaches. Remember, accuracy today prevents issues tomorrow. By adhering to these guidelines, you'll be better positioned to navigate the complexities of tax reporting for your business.

Filing taxes can often leave you scratching your head, especially when you're dealing with specific forms like the IRS Schedule C (Form 1040). This form, pivotal for reporting income or loss from a business you operated or a profession you practiced as a sole proprietor, is surrounded by misconceptions. Here, we'll debunk some common misunderstandings to provide clarity on this crucial aspect of tax filing.

Misconception #1: Schedule C is only for full-time business owners. Many people believe that you need to be running a business full-time to use Schedule C. However, even if you're involved in a side gig or a part-time business, you're required to report this income using Schedule C as long as you're pursuing the activity with a profit motive.

Misconception #2: All expenses are deductible if they're business-related. While Schedule C allows for a wide range of business expenses to be deducted, not all costs are automatically deductible. Expenses must be both "ordinary and necessary" for your business to qualify. Personal expenses and capital expenses, for example, are treated differently.

Misconception #3: Hobby income shouldn't be reported on Schedule C. The distinction between a hobby and a business might seem blurry, but for tax purposes, it's crucial. If you engage in an activity primarily for profit, it's a business, and you should report income or loss on Schedule C. Income from hobbies, on the other hand, is reported differently, and you can't deduct expenses in the same way.

Misconception #4: You don't have to report small amounts of income. Some believe that there's a threshold below which income doesn't need to be reported. In reality, all income must be reported, regardless of amount. Failing to report even small amounts could lead to penalties.

Misconception #5: Home office deductions are a red flag for audits. A common belief is that claiming a home office deduction significantly increases your chances of an IRS audit. While it's important to legitimately qualify for this deduction according to IRS rules, the mere act of claiming it doesn't automatically trigger an audit.

Misconception #6: Schedule C filers can't take the standard deduction. Another widespread misconception is that if you file Schedule C, you're ineligible for the standard deduction on your personal tax return. In fact, business income reported on Schedule C is separate from, and doesn't affect, your eligibility for the standard deduction.

Misconception #7: You must have a formal business structure to file Schedule C. Some people think that an official business entity, like an LLC or corporation, is required to file Schedule C. However, sole proprietors without any formal business structure can (and must) file Schedule C to report their business income.

Misconception #8: Only goods sold count as income. This misunderstanding can lead to underreporting of income. In reality, all forms of income, including services provided, are considered business income and must be reported on Schedule C.

Understanding the truths behind these misconceptions can help demystify the process of filing Schedule C and ensure that you stay on the right side of tax laws. If you're ever in doubt, consulting with a tax professional can offer personalized guidance tailored to your specific situation.

When dealing with the IRS Schedule C 1040 form, it's crucial to gather a comprehensive understanding to ensure accurate reporting of business income and expenses. This form is integral for anyone who operates a sole proprietorship or single-member LLC, detailing the profits and losses of the business. Here are some key takeaways to consider:

Properly completing the IRS Schedule C 1040 form is essential for accurately reporting your business earnings and deductions. Taking the time to understand and carefully fill out this form can not only help you comply with tax laws but also minimize your tax liability, thus benefiting your business in the long run.

Profits or Loss From Business - Tax preparers often help to identify additional deductions and credits you might miss when filling out this form on your own.

Baseball Evaluation Form - Facilitates detailed record-keeping that can track player improvement over time.