Printable Vehicle Repayment Agreement Template

Printable Vehicle Repayment Agreement Template

When purchasing a vehicle, the financial aspect can often become a complex affair, especially when loans or financing plans are involved. A Vehicle Repayment Agreement form becomes an essential document in these situations, serving as a formal agreement between the borrower and the lender. This agreement outlines the specifics of the repayment plan for the vehicle, detailing the loan amount, interest rate, repayment schedule, and the consequences of failing to meet these terms. The form not only provides a structured and clear path for repaying the vehicle but also serves to protect the rights and interests of both parties involved. It ensures that the borrower is aware of their financial obligations, while giving the lender a legal framework to enforce the agreement, should there be any issues with repayments. By providing a detailed outline of the loan's conditions, the Vehicle Repayment Agreement form plays a pivotal role in making the process of financing a vehicle transparent, manageable, and secure for all parties involved.

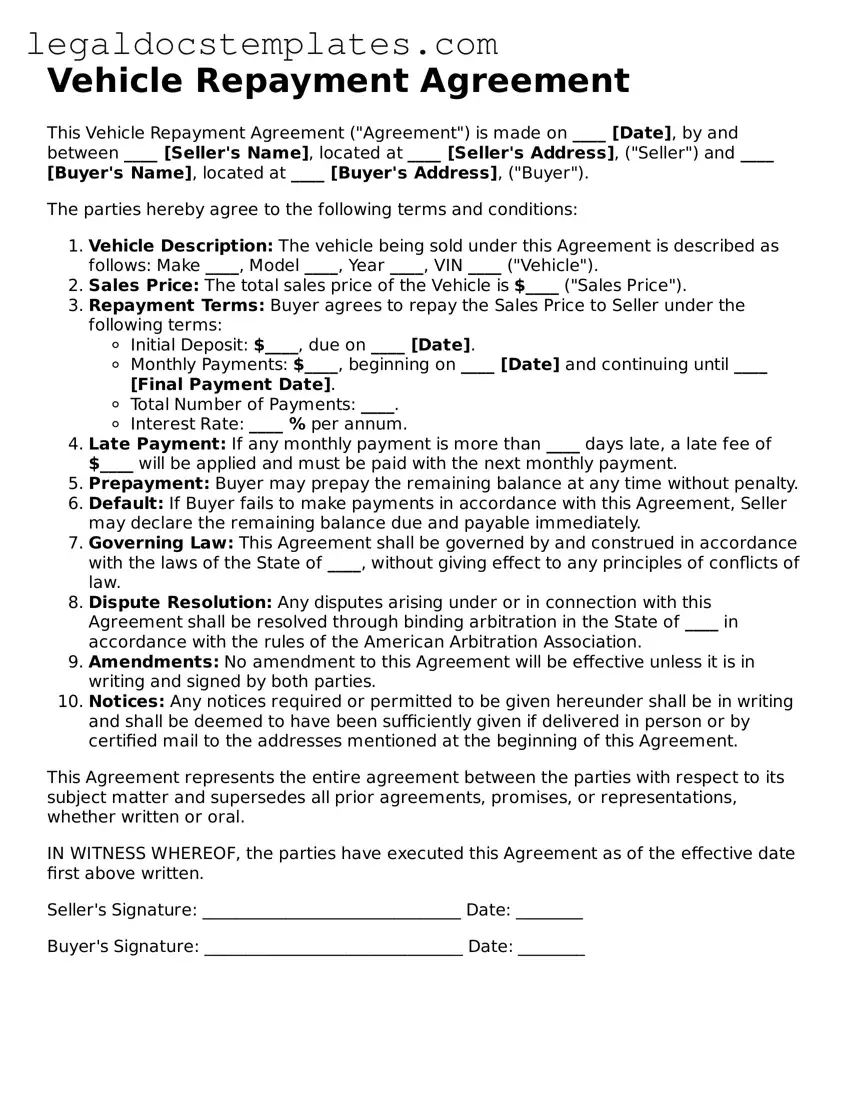

Vehicle Repayment Agreement

This Vehicle Repayment Agreement ("Agreement") is made on ____ [Date], by and between ____ [Seller's Name], located at ____ [Seller's Address], ("Seller") and ____ [Buyer's Name], located at ____ [Buyer's Address], ("Buyer").

The parties hereby agree to the following terms and conditions:

This Agreement represents the entire agreement between the parties with respect to its subject matter and supersedes all prior agreements, promises, or representations, whether written or oral.

IN WITNESS WHEREOF, the parties have executed this Agreement as of the effective date first above written.

Seller's Signature: _______________________________ Date: ________

Buyer's Signature: _______________________________ Date: ________

| Fact | Description |

|---|---|

| Purpose | The Vehicle Repayment Agreement form is used to establish the terms under which a borrower agrees to repay a loan that was used to purchase a vehicle. |

| Components | It typically includes details such as the loan amount, interest rate, repayment schedule, and the rights and responsibilities of both the borrower and the lender. |

| Governing Law | The agreement is governed by the state laws where it is executed. Specific provisions and requirements can vary significantly from one state to another. |

| Secured Loan | Most vehicle repayment agreements are secured loans, meaning the vehicle itself serves as collateral to secure the loan in case the borrower defaults. |

| Default Consequences | If the borrower defaults on the agreement, the lender may have the right to repossess the vehicle. |

| Modification | Any modifications to the agreement after it has been signed must be agreed upon in writing by both the borrower and the lender. |

| Prepayment | The agreement may include terms regarding prepayment, including whether the borrower can pay off the loan early and if any penalties apply. |

| Importance of Review | Both parties should thoroughly review the agreement before signing to ensure it accurately reflects the terms of their understanding. |

Entering into a Vehicle Repayment Agreement is a significant step that helps ensure clarity and commitment from both the lender and the borrower regarding the terms of paying back a loan used to purchase a vehicle. It serves as a formal arrangement that outlines the repayment schedule, interest rates, and the consequences of failing to adhere to the agreed terms. To make this process smoother, it’s crucial to accurately fill out the Vehicle Repayment Agreement form. Follow the steps outlined below to complete the form correctly.

Once the Vehicle Repayment Agreement form is fully completed and signed, both the borrower and the lender should keep a copy for their records. This document serves as a legally binding contract that both parties can refer to, ensuring transparency and understanding throughout the repayment process.

A Vehicle Repayment Agreement is a legal contract between two parties, typically involving the buyer and seller of a vehicle. This agreement outlines the terms and conditions under which the buyer agrees to pay back the seller or a financing company for the vehicle. It includes details such as payment amounts, schedules, interest rates, and the consequences of failing to make payments as agreed.

A Vehicle Repayment Agreement is crucial because it legally binds the parties to the terms of the repayment. This serves to protect both the buyer and seller by ensuring there is a clear understanding of the repayment plan. It can help avoid disputes over payments and ensure that the seller or lender can take certain actions if payments are not made as scheduled.

Yes, a Vehicle Repayment Agreement can be modified, but any changes must be agreed upon by both parties. Modifications should be documented in writing and attached to the original agreement. Both parties should sign or initial any amendments to ensure that the changes are legally enforceable.

If a payment is missed, the consequences outlined in the agreement will apply. Typically, this could involve late fees, additional interest charges, and, in some cases, the initiation of repossession procedures for the vehicle. It's essential to communicate with the lender or seller immediately if you anticipate missing a payment to discuss potential solutions or accommodations.

While the specifics can vary, Vehicle Repayment Agreements are generally considered legally binding contracts across all states. However, the enforceability of certain conditions and the exact legal remedies available may differ from one state to another. For this reason, it's advisable to consult with a legal advisor familiar with your state's laws to ensure your agreement is fully compliant.

Templates for a Vehicle Repayment Agreement can be found online through legal services websites, at local libraries, or by consulting with a legal professional. It's important to choose a template that is current and compliant with your state's laws. Personalizing the template to fit the specific terms of your agreement is also crucial to ensure all aspects of the deal are covered.

When filling out a Vehicle Repayment Agreement form, a common mistake is not accurately identifying the parties involved. This mistake can lead to confusion about who is responsible for repaying the loan and who owns the vehicle until the loan is fully repaid. It is crucial that full names, addresses, and contact information for both the borrower and the lender are clearly stated to avoid any misunderstandings.

Another error often encountered is the failure to specify the vehicle details precisely. For an agreement to be enforceable, it must clearly describe the vehicle, including make, model, year, color, VIN (Vehicle Identification Number), and mileage. This level of detail ensures that there is no ambiguity about which vehicle is subject to the repayment agreement.

Many individuals neglect to outline the loan terms clearly. This includes specifying the loan amount, interest rate (if any), repayment schedule, and the total number of payments to be made. Clarifying these details upfront can prevent disputes over the amount owed or the duration of the repayment period. Without this clarity, either party may mistakenly believe the terms are different than agreed upon, leading to potential legal complications.

Not defining the repercussion for late payments or defaults is a mistake that can significantly impact the lender. It's essential to stipulate what will happen if the borrower fails to make payments on time, including any late fees or the possibility of repossession. This holds the borrower accountable and provides a clear course of action should they fail to meet their obligations.

Overlooking the need for a witness or notary to sign the agreement is another common oversight. While not always legally required, having the agreement witnessed or notarized can add an extra layer of legitimacy and may help in enforcing the agreement if there's a dispute. This simple step can provide valuable legal protection to both parties.

Failure to include a clause that addresses modifications to the agreement is a critical error. Circumstances change, and the agreement might need to be updated. Without a modification clause, changes can be difficult to enforce or may require drafting a new agreement entirely. This clause ensures that agreed-upon changes are legally recognized.

Ignoring state-specific requirements can also lead to issues. Each state may have unique laws regarding vehicle repayment agreements, including specific disclosures or terms that need to be included. Not researching and adhering to these requirements can render the agreement invalid or unenforceable in a legal dispute.

A common and potentially costly mistake is not keeping a signed copy of the agreement. Both parties should have a copy of the fully executed agreement for their records. This ensures that there is evidence of the contract and its terms, which is crucial if there's a misunderstanding or if the matter ever goes to court.

When dealing with a Vehicle Repayment Agreement, it's crucial to have a holistic view of all related documents to ensure all legal and financial bases are covered. This agreement is just one part of a larger ensemble of documents that safeguard interests and clarify terms between parties involved in the sale, purchase, or financing of a vehicle. Here's a list of other forms and documents often used alongside the Vehicle Repayment Agreement, each serving a unique but interconnected function.

To sum up, understanding and managing the documents associated with a Vehicle Repayment Agreement is vital for a smooth, legally compliant transaction. This encompasses everything from verifying ownership and insurance to assessing financial worthiness and registering the vehicle with state authorities. Having these documents in order provides a clear path forward for both buyers and sellers and ensures that all parties are protected throughout the process.

The Personal Loan Agreement form resembles the Vehicle Repayment Agreement in terms of structure and purpose. Both documents are designed to lay down the terms under which money is lent by one party to another, specifying repayment schedules, interest rates, and consequences of default. However, the Personal Loan Agreement is broader in scope, potentially covering a wide range of personal loans beyond vehicle financing. This includes loans for education, healthcare, or other personal expenditures, making it versatile yet fundamentally similar in securing a lender's investment.

Lease Agreements share common ground with Vehicle Repayment Agreements, primarily in the establishment of a fixed-term arrangement between two parties. In a Lease Agreement, one party agrees to rent property (real estate, equipment, vehicles) to another party for a specified period, often detailing payment intervals, maintenance responsibilities, and termination clauses. Like Vehicle Repayment Agreements, these documents protect both parties' interests but focus on the temporary use of an asset rather than financing its purchase.

The Installment Sale Agreement has a direct correlation with the Vehicle Repayment Agreement, as both facilitate the purchase of an item through scheduled payments. These agreements lay out the total purchase price, down payment, interest rates, payment schedule, and the repercussions of failing to keep up with payments. The key difference lies in the Installment Sale Agreement’s broader applicability to various items, such as real estate or business assets, while maintaining a similar legal framework to ensure payment completion over time.

The Promissory Note echoes elements of the Vehicle Repayment Agreement by recording a debt and promising repayment under specific terms. This document is simpler, focusing on the essentials of the amount borrowed, interest rate, repayment schedule, and the borrower's signature. While it can be used for a variety of loans, including vehicle loans, it lacks the detailed terms regarding the specific nature of the loan's use and collateral, which might be included in a more detailed Vehicle Repayment Agreement. Nevertheless, its fundamental principle of documenting a commitment to repay a debt aligns closely with the intentions behind the Vehicle Repayment Agreement.

Credit Card Agreements also parallel the Vehicle Repayment Agreement in the structure of debt repayment. These agreements outline the terms under which credit is extended to the purchaser, encompassing interest rates, minimum payment requirements, and fees for late payments, much like the Vehicle Repayment Agreement outlines repayment for a vehicle. However, Credit Card Agreements are inherently revolving, allowing for continuous borrowing within a credit limit, contrasting the closed-end nature of a vehicle repayment, which is for a fixed amount and period until the debt is fully repaid.

Filling out a Vehicle Repayment Agreement form is a critical step in securing a fair and legal arrangement for repaying a loan used to purchase a vehicle. It is crucial to approach this process thoughtfully and meticulously to ensure both parties understand their responsibilities and rights. Below are seven dos and don'ts to consider when completing this form:

Do:Read the entire form thoroughly before writing anything. Understanding every section ensures you know what information is required and helps prevent mistakes.

Use clear and legible handwriting if filling out the form by hand. This prevents misunderstandings or issues due to illegibility.

Provide accurate information about both the borrower and the lender, including full names, addresses, and contact details. Accuracy in these details is crucial for legal validity.

Detail the loan amount, interest rate (if applicable), repayment schedule, and any late fees clearly. These are key terms that affect both parties significantly.

Have all parties sign and date the form in the presence of a notary public, if possible. This step can add an extra layer of legal protection and validity.

Keep a copy of the agreement in a safe place. Both the borrower and the lender should have a copy for their records.

Consult with a legal professional if there are any uncertainties. Getting professional advice can prevent legal issues down the road.

Rush through the process without understanding each section. Taking the time to comprehend every part of the agreement is essential.

Omit any details about the repayment terms. Leaving out information can lead to disputes or misunderstandings in the future.

Use vague language. Be as specific as possible to avoid ambiguity. This includes specifying dates, amounts, and any conditions clearly.

Forget to specify what happens if the borrower defaults. Both parties should understand the consequences and processes if the borrower fails to make payments.

Sign the agreement if any doubts or disagreements about its content exist. Ensure all parties are fully agreeable to each term before proceeding.

Ignore any state-specific legal requirements. The laws governing these agreements can vary, so it's important to ensure compliance with local regulations.

Alter the agreement after it has been signed without written consent from all parties. Any modifications should be agreed upon, documented, and signed by everyone involved.

Understanding the Vehicle Repayment Agreement form is crucial for anyone involved in the purchase or sale of a vehicle on terms. This document outlines how the buyer will pay the seller for the vehicle over time. However, there are common misconceptions that can lead to confusion or even legal issues if not addressed properly. Here are eight of the most frequent misunderstandings:

Understanding these misconceptions and the true nature of the Vehicle Repayment Agreement can ensure a smoother transaction for both parties, preventing future disputes and fostering a clearer legal relationship from the start of the purchasing process.

When entering an agreement centered around vehicle repayment, clarity and thoroughness are paramount. Both parties—the owner and the borrower—must have a mutual understanding and set clear expectations through documentation. Here are five key takeaways to consider when filling out and utilizing a Vehicle Repayment Agreement form:

Adhering to these guidelines while filling out and using the Vehicle Repayment Agreement form can safeguard the interests of all involved parties. It turns a verbal agreement into an enforceable document, promoting accountability and preventing potential conflicts.

How Do I Get My P45 - HMRC can make special arrangements if an employee wishes to keep their P45 details private from a new employer.

Corrective Deed California - It reflects a pragmatic approach to problem-solving within the legal framework, emphasizing accuracy and integrity in documentation.

Peco Energy - Load characteristics including connected load, maximum summer and winter demand must be completed.