Fill Out Your Profit And Loss Template

Fill Out Your Profit And Loss Template

In the bustling world of business, understanding the financial health of an enterprise is paramount. One key document that offers insights into this aspect is the Profit and Loss form, often abbreviated as P&L. This crucial form provides a comprehensive snapshot of a company's revenue, costs, and expenses over a specific period, usually quarterly or annually. Its primary purpose is to elucidate whether a company has made a profit or incurred a loss during the designated time frame. By detailing the total income and subtracting the expenses necessary to operate, the form highlights the net profit or loss. This invaluable tool not only aids business owners and investors in making informed decisions but also plays a critical role in the strategic planning and forecasting of future endeavors. Furthermore, it is essential for tax reporting and compliance, showcasing its multifaceted importance in the financial realm.

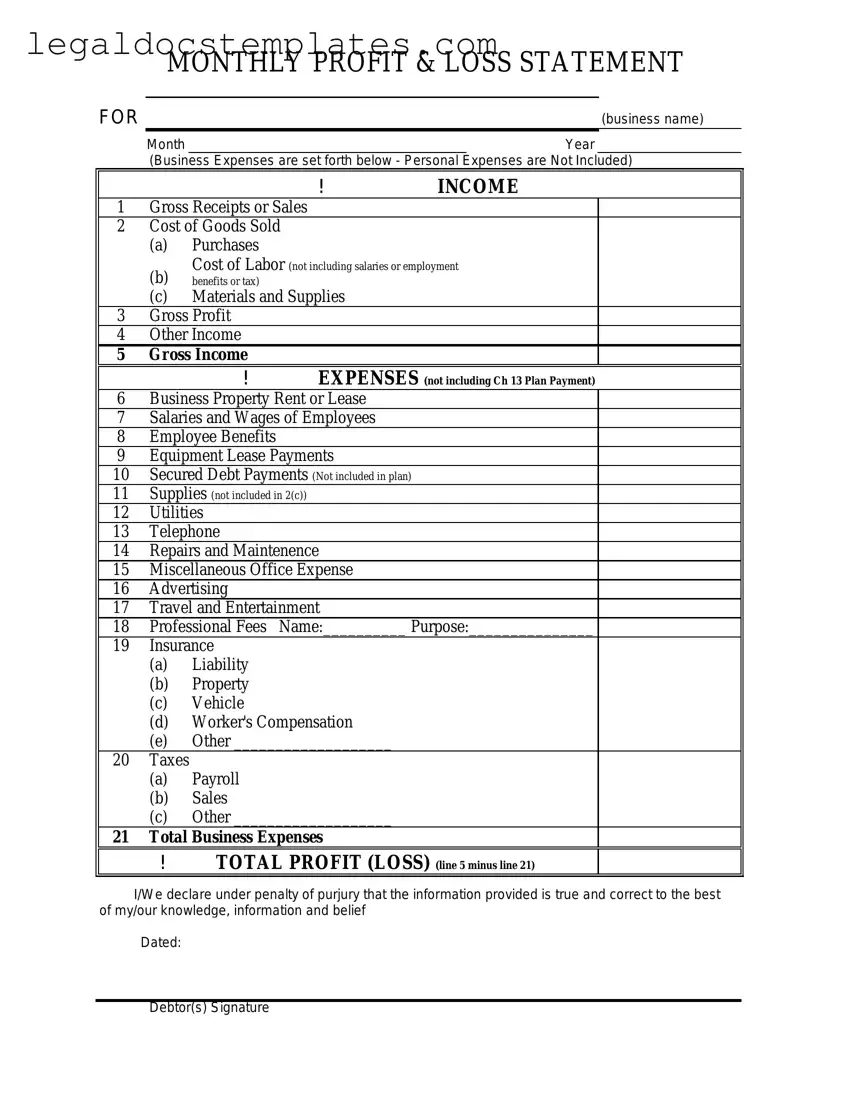

MONTHLY PROFIT & LOSS STATEMENT

FOR |

(business name) |

Month |

Year |

(Business Expenses are set forth below - Personal Expenses are Not Included)

|

|

|

! |

INCOME |

1 |

Gross Receipts or Sales |

|

||

2 |

Cost of Goods Sold |

|

||

|

(a) |

Purchases |

|

|

|

(b) |

Cost of Labor (not including salaries or employment |

||

|

benefits or tax) |

|

|

|

|

(c) |

Materials and Supplies |

|

|

3 |

Gross Profit |

|

|

|

4 |

Other Income |

|

|

|

5 |

Gross Income |

EXPENSES (not including Ch 13 Plan Payment) |

||

|

|

! |

||

6 |

Business Property Rent or Lease |

|

||

7 |

Salaries and Wages of Employees |

|

||

8 |

Employee Benefits |

|

|

|

9 |

Equipment Lease Payments |

|

||

10 |

Secured Debt Payments (Not included in plan) |

|

||

11 |

Supplies (not included in 2(c)) |

|

||

12 |

Utilities |

|

|

|

13 |

Telephone |

|

|

|

14 |

Repairs and Maintenence |

|

||

15 |

Miscellaneous Office Expense |

|

||

16 |

Advertising |

|

|

|

17 |

Travel and Entertainment |

|

||

18 |

Professional Fees |

Name:__________ Purpose:_______________ |

||

19 |

Insurance |

|

|

|

|

(a) |

Liability |

|

|

|

(b) |

Property |

|

|

|

(c) |

Vehicle |

|

|

|

(d) |

Worker's Compensation |

|

|

|

(e) |

Other ___________________ |

|

|

20 |

Taxes |

|

|

|

|

(a) |

Payroll |

|

|

|

(b) |

Sales |

|

|

|

(c) |

Other ___________________ |

|

|

21 |

Total Business Expenses |

|

||

|

! |

TOTAL PROFIT (LOSS) (line 5 minus line 21) |

||

I/We declare under penalty of purjury that the information provided is true and correct to the best of my/our knowledge, information and belief

Dated:

Debtor(s) Signature

| Fact Name | Description |

|---|---|

| Purpose | A Profit and Loss (P&L) form is used by businesses to summarize revenue, costs, and expenses incurred during a specific period of time, usually a fiscal quarter or year. |

| Also Known As | It is also referred to as an Income Statement, Statement of Income, or Statement of Operations. |

| Key Components | Typical components include gross revenue, cost of goods sold (COGS), gross profit, operating expenses, net income before taxes, and net income. |

| Importance for Businesses | This form is crucial for businesses as it provides insights into the company's financial performance, helping in making informed decisions. |

| User Base | Utilized by businesses of all sizes, from sole proprietors to multinational corporations. |

| Frequency of Use | Most businesses prepare a P&L statement quarterly and annually, though it can be compiled more frequently for internal use. |

| Governing Laws | While specific to each state, general principles of accounting standards such as the Generally Accepted Accounting Principles (GAAP) in the U.S. guide its preparation. |

| Variability by Industry | The structure and emphasis of a P&L form can vary significantly by industry due to different operational, cost, and revenue factors. |

| Accessibility | Accounting software and templates make it easier for businesses to prepare their P&L statements, even without extensive accounting knowledge. |

| Impact on Tax Filing | The information from a P&L statement is essential for tax preparation and filing, as it provides a detailed account of taxable income. |

Filling out a Profit and Loss (P&L) form is a crucial step for businesses of all sizes to assess their financial health over a specific period. This document captures both the revenues and the expenses incurred, thereby helping in understanding profitability. It serves as a foundational piece of financial reporting that can guide decision-making and strategy for business growth. The following step-by-step instructions aim to simplify the process, ensuring accuracy and completeness in filling out the P&L form.

Once the P&L form is filled out accurately, it serves as a vital tool for assessing the business's financial performance, aiding in strategic planning and future financial forecasting. By regularly completing this form, businesses can identify trends, make informed decisions, and implement strategies for improved profitability and growth.

A Profit and Loss (P&L) form is a financial statement that summarizes the revenues, costs, and expenses incurred during a specific period, usually a fiscal quarter or year. This document, also known as an income statement, helps stakeholders understand whether a company made a profit or incurred a loss during the period reported. It reflects the company's operational efficiency and is used for both internal management and external reporting.

The requirement to fill out a Profit and Loss form applies to various entities, including:

To accurately prepare a Profit and Loss form, the following information is necessary:

The frequency at which a business should prepare a Profit and Loss statement can vary, but typically includes:

Filling out a Profit and Loss (P&L) form can be a daunting task, especially for those new to handling their business finances. A common mistake many people make is not thoroughly understanding what qualifies as revenue. Revenue isn't just the cash that enters your business; it encompasses all income earned, even if not yet received. This oversight can lead to an inaccurate portrayal of a business's financial health.

Another area where errors frequently occur is in the classification of expenses. Not all costs a business incurs are direct expenses. Some are indirect, such as administrative costs and general overhead. Mixing these up can distort the true cost of goods sold and, as a result, the gross profit margin. Keeping these categories distinct is crucial for an accurate P&L statement.

Often, businesses fail to account for depreciation and amortization, leading to an overestimation of profit. These non-cash expenses reduce the value of assets over time and must be included to reflect the actual earning power of the business. Ignoring them can paint an overly optimistic picture of financial health.

Underestimating or forgetting to include all operating expenses is yet another common pitfall. Operating expenses are the costs associated with running the daily business operations. Missing out on these can significantly impact the net profit figure. It's essential to comb through all expenses meticulously to ensure completeness.

A crucial but sometimes overlooked component is the recognition of accrued expenses. These are expenses that have been incurred but not yet paid. A failure to include these can inflate profit figures, leaving stakeholders with a misleading representation of the company's financial position.

Many also err by mixing business and personal expenses. This not only complicates the P&L statement but can also lead to tax complications. Keeping personal transactions separate from business accounts is fundamental to maintaining clear and accurate financial records.

Not regularly updating the P&L statement is a mistake that can have far-reaching consequences. A P&L statement should be a living document, reflecting the current state of the business. Infrequent updates can hinder decision-making and obscure the business's true performance trajectory.

Another error lies in the misunderstanding of the difference between profit and cash flow. A P&L statement measures a company's profitability, not its cash holdings. Confusing the two can lead to misguided business decisions, such as assuming there's ample cash to cover expenditures when there isn't.

Finally, attempting to complete the P&L form without seeking professional advice can result in numerous inaccuracies. Tax laws and financial reporting standards are complex and subject to change. Professional guidance ensures your P&L statement complies with current regulations and accurately reflects your business's financial health.

By avoiding these common mistakes, individuals can produce more accurate and useful Profit and Loss statements, paving the way for informed financial decision-making and, ultimately, a more successful business operation.

When handling financial matters, particularly for businesses or self-employed individuals, the Profit and Loss (P&L) form is crucial. However, to get a comprehensive understanding of a business's financial health, this form is often accompanied by several other important documents. Each of these documents plays a vital role in painting the full picture of financial standing, making decision-making more informed.

Together with the Profit and Loss form, these documents create a comprehensive financial report that can be used for both internal assessments and external reporting. Understanding each document’s unique role can significantly impact strategic planning, financial management, and compliance efforts. Therefore, being familiar with these documents is vital for anyone involved in managing or assessing a business's financial health.

The Balance Sheet is quite similar to the Profit and Loss form, as both are crucial financial statements for any business. While the Profit and Loss form focuses on the income and expenses over a period, revealing the net income, the Balance Sheet provides a snapshot of a company's financial condition at a specific point in time. It lists assets, liabilities, and owners’ equity, offering a broader view of financial health. Together, they give stakeholders insight into profitability and financial stability.

Another document resembling the Profit and Loss form is the Cash Flow Statement. Both documents are essential for understanding a business's financial operations, but they serve different purposes. The Profit and Loss form details the company's revenues, costs, and expenses to show its profitability. Meanwhile, the Cash Flow Statement tracks the flow of cash in and out of a business, highlighting its liquidity. This statement categorizes cash flows into operating, investing, and financing activities, providing a clear picture of how the company earns and spends its cash over time.

The Income Statement is often used interchangeably with the Profit and Loss form, and they essentially serve the same purpose, which is to demonstrate a company's financial performance over a specific period. They detail revenues, expenses, and profits or losses, showing how operational and non-operational activities impact the overall financial result. However, "Profit and Loss" is more commonly used in colloquial speech, whereas "Income Statement" is the term preferred in formal accounting contexts.

Statement of Retained Earnings is another document that has similarities with the Profit and Loss form, although it focuses on a different aspect of financial reporting. This statement explains changes in a company’s retained earnings over a period, often linking directly to the net income reported on the Profit and Loss form. It shows how much profit is reinvested in the business versus distributed to shareholders as dividends. Thus, it gives insights into a company’s dividend policy and growth strategy by detailing the accumulation of profits.

The Budget Report shares similarities with the Profit and Loss form by presenting financial data that can inform decision-making and performance evaluation. While the Profit and Loss form records actual income and expenditure over a period, showing the net profit or loss, a Budget Report outlines the financial plan for the future, including projected revenues and expenses. Comparing these actual and projected figures enables businesses to manage their finances more effectively, spot trends, and make adjustments as necessary.

Finally, the Break-even Analysis is related to the Profit and Loss form in that both are used to evaluate a business's financial performance and viability. The Break-even Analysis calculates the point at which total revenues equal total costs, and the business neither makes a profit nor incurs a loss. It helps in understanding how changes in price levels, costs, and volume affect profitability. In contrast, the Profit and Loss form provides a detailed record of past financial activity, showing the actual profit or loss achieved in a given period.

Navigating through the intricacies of financial documents can feel like walking through a maze, especially when it's time to tackle the Profit and Loss (P&L) form. A clear, well-prepared P&L form not only reflects the financial health of a company over a specific period but also plays a crucial role in decision-making processes for businesses. Here are some essential dos and don'ts to help guide you through filling out this important document.

Do:The Profit And Loss (P&L) form, often misunderstood, is a fundamental financial statement that outlines a company's revenues, costs, and expenses during a specific period. Despite its importance, several misconceptions surround its purpose and use. Below are seven common myths demystified:

Only Accountants Need to Understand It: While accountants are experts in financial statements, the P&L form is crucial for business owners, managers, and investors to understand. It provides valuable insights into the financial health and operational performance of the business, guiding decision-making.

It Shows the Exact Cash Position of a Business: The P&L form tracks revenue and expenses, which may not always represent cash transactions. For example, sales made on credit are recorded as revenue even though cash hasn’t been received yet, and similarly for expenses incurred but not paid in cash.

Revenue Is the Same as Profit: A common misunderstanding is equating total revenue with profit. Revenue is the total income before any deductions, whereas profit is what remains after all operating expenses, taxes, and interest have been subtracted from total revenue.

A Positive P&L Always Means the Business Is Financially Healthy: A positive P&L indicates that revenue exceeds expenses; however, it does not account for cash flow issues, such as the timing of receiving payments and making payments, which can affect the business's financial health.

P&L Is Only for Internal Use: While primarily used by management to make financial decisions, the P&L form is also important for external parties. Investors, lenders, and other stakeholders review this document to evaluate a company’s performance and financial stability.

All Expenses Are Deducted at Once: It's a misconception that all expenses are fully deducted in the period they are incurred. Some expenses, like the purchase of long-term assets, are capitalized and then depreciated over time, affecting the P&L across multiple periods.

It’s Only Prepared Annually: While an annual P&L is common, businesses often prepare it monthly or quarterly. Frequent preparation allows for better tracking of financial performance, making it easier to adjust strategies promptly and manage finances effectively.

The Profit And Loss (P&L) form is an essential financial document that provides a comprehensive overview of a company's revenues, expenses, and net income over a specific period. Understanding how to properly fill out and utilize this form can greatly benefit businesses in managing their finances effectively. Here are five key takeaways:

Printable Medication Mar Sheet - An essential document for caregivers to manage and report the administration of medications across different hours of the day.

Doctors Return to Work Note - It describes how the work release will be managed, including supervision and tracking of the individual.

Form I-983 - Failure to fully complete or timely submit the I-983 form can lead to serious legal implications for both the student and the employer.