Fill Out Your Mortgage Statement Template

Fill Out Your Mortgage Statement Template

Understanding the complexities surrounding a Mortgage Statement form is crucial for homeowners in effectively managing their home loan. This document, provided by the mortgage servicer, serves as a comprehensive overview of the loan account, including vital details such as the servicer's contact information, borrower's name and address, and a breakdown of the mortgage payment due. Key components such as the statement date, account number, due date for the next payment, and the amount due including any late fee charges if the payment is made past the due date, are outlined for the homeowner's convenience. Besides detailing the outstanding principal and interest rates, it mentions whether a prepayment penalty is applicable and provides a thorough explanation of the amount due, segregating it into principal, interest, and escrow amounts for taxes and insurance. An account of transaction activity within a specified period highlights charges, payments received, and fees, giving a transparent view of the account's activity. Importantly, the form alerts borrowers about partial payments, their treatment, any delinquency notices which caution homeowners about the repercussions of late payments including potential foreclosure, and offers guidance on what steps to take if facing financial difficulties. This detailed statement plays a pivotal role in keeping homeowners informed about their mortgage status, enabling them to make timely decisions and manage their mortgage responsibility with full awareness.

[Servicer Name]

Customer Service: [PHONE NUMBER] [WEBSITE]

[Borrower Name and Address]

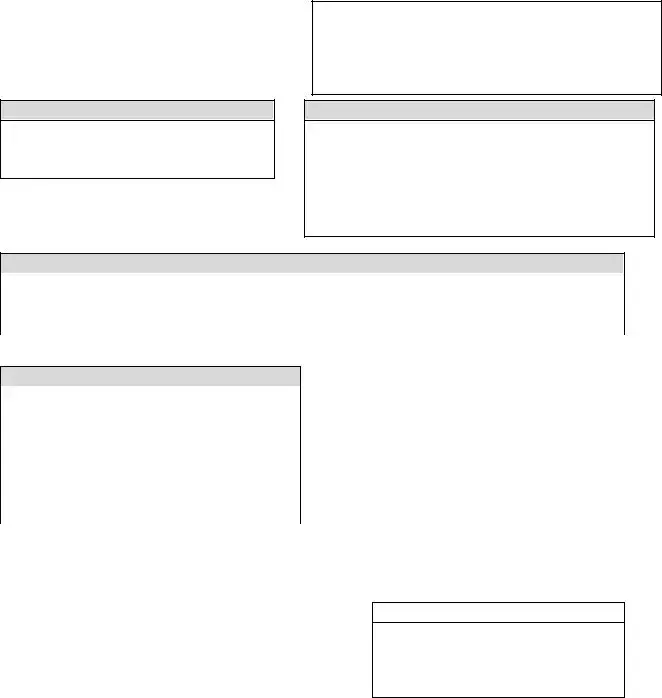

Mortgage Statement

Statement Date: _______

Account Number |

____________ |

Payment Due Date |

____________ |

Amount Due |

____________ |

If payment is received after [DATE], $____ late fee will be charged.

Account Information

Outstanding Principal |

$_______ |

Interest Rate (Until [Date]) |

______% |

Prepayment Penalty |

[Yes/No] |

Explanation of Amount Due

Principal |

$_______ |

Interest |

$_______ |

Escrow (for Taxes and Insurance) |

$_______ |

Regular Monthly Payment |

$_______ |

Total Fees Charged |

$_______ |

Total Amount Due |

$_______ |

Transaction Activity (_/_/_ [Date] to _/_/_ [Date])

Date |

Description |

Charges |

Payments |

[Date] |

Late Fee (charged because full payment not received by _/_/_ |

$ |

|

[Date] |

Payment Received – Thank you |

|

$ |

[Date] |

Fee Description |

$ |

|

Past Payments Breakdown

|

Paid |

Paid |

|

Last |

Year to |

|

Month |

Date |

Principal |

$ |

$ |

Interest |

$ |

$ |

Escrow (Taxes and Insurance) |

$ |

$ |

Fees |

$ |

$ |

Total |

$ |

$ |

[Servicer Name and Address]

Amount Due

Due By _/_/_ [Date]$

$___ late fee will be charged after [Date]

Additional Principal |

$ |

Additional Escrow |

$ |

Total Amount Enclosed |

$ |

Make check payable to [Servicer Name]

[Account Number]

[Additional tables to be translated]

Important Messages

*Partial Payments: Any partial payments that you make are not applied to your mortgage, but instead are held in a separate suspense account. If you pay the balance of a partial payment, the funds will then be applied to your mortgage.

**Delinquency Notice**

You are late on your mortgage payments. Failure to bring your loan current may result in fees and foreclosure – the loss of your home. As of [Date], you are __ days delinquent on your mortgage loan.

Recent Account History

·Payment due [Date]: Fully paid on time

·Payment due [Date]: Fully paid on [Date]

·Payment due [Date]: Unpaid balance of $________

·Current payment due [Date]: $_______

·Total: $_______ due. You must pay this amount to bring your loan current.

If you are Experiencing Financial Difficulty: See back for information about mortgage counseling or assistance.

| Fact Name | Fact Detail |

|---|---|

| Contact Information | The mortgage statement includes the servicer's name, customer service phone number, and website for borrower inquiries. |

| Borrower Information | It lists the borrower's name and address, providing a personal touch to the mortgage statement. |

| Payment Information | Details such as the statement date, account number, payment due date, and total amount due are clearly presented. |

| Late Payment Policy | If the payment is received after a specified date, a late fee is charged, emphasizing the importance of timely payments. |

| Account Information | Includes key figures such as outstanding principal, interest rate, and any prepayment penalty enabling borrowers to see the details of what they owe and why. |

| Explanation of Amount Due | The statement breaks down the total amount due into principal, interest, and escrow for taxes and insurance, plus any regular monthly payment or total fees charged. |

| Transaction Activity | Lists all transactions within a certain period, including dates, descriptions, charges, and payments made or incurred. |

| Special Messages | Contains important notices about partial payments, delinquency warnings, payment history, and information on financial difficulty assistance. |

Filling out a Mortgage Statement form is a crucial step for homeowners managing their mortgage payments and understanding their financial status regarding their home loan. This document provides a detailed summary of the outstanding amount, payment history, and other relevant financial details concerning the mortgage. To ensure accuracy and avoid any potential issues with your mortgage servicer, following the steps below carefully is important.

After the Mortgage Statement form is carefully filled out and submitted, your mortgage servicer will process the information to update your loan account. This form plays a key role in ensuring the proper application of your payments and the accurate calculation of your outstanding balance. Keep a copy of this completed form for your records, and consider following up with your servicer if you have questions or if any significant changes happen in your financial situation. Remember, staying informed and proactive about your mortgage payments helps maintain your financial health and peace of mind.

A mortgage statement is a document provided by your loan servicer that gives you details about your mortgage at a specific point in time. This statement includes the outstanding principal, interest rate, payment due date, amount due, account activity, and more. It gives a clear snapshot of your loan's current status, including any fees charged and breakdowns of payments towards principal, interest, and escrow.

The payment due date on your mortgage statement indicates the deadline by which you should make your monthly loan payment. If payments are received after this date, the lender may charge a late fee as specified in your statement. Prompt payments are crucial to avoid additional charges and to keep your loan in good standing.

The 'Escrow' section of your mortgage statement details the amount collected and used to pay for taxes and insurance on your behalf. These funds are held in an escrow account by your servicer and are used to ensure that your property taxes and homeowners insurance premiums are paid on time, avoiding any lapses in coverage or delinquencies.

Partial payments made towards your mortgage are not directly applied to your loan amount. Instead, they are placed in a separate suspense account until the balance of the partial payment is paid off. Once the complete payment is made, the funds are then applied to your mortgage. This policy ensures that payments towards the principal, interest, and escrow are properly managed.

A 'Delinquency Notice' is a warning included in your mortgage statement indicating that your loan payments are overdue. The notice outlines how many days you are delinquent, the risks associated with continued non-payment (such as fees and foreclosure), and the total amount due needed to bring your loan current. Immediate action is advised to address the situation and avoid further consequences.

If you are experiencing financial difficulties and need help with your mortgage, your statement includes guidance on where to find mortgage counseling or assistance. This information is usually found on the back of the statement and can provide you with the necessary resources to explore options available for managing your mortgage payments and avoiding foreclosure.

Filling out a Mortgage Statement form is an important task, yet people often make mistakes that can have significant consequences. One common error is inaccurately entering the Borrower Name and Address. It might seem simple, but any discrepancy in this information can lead to delays or mix-ups in communication between the mortgage servicer and the borrower.

Another area often filled out incorrectly is the Statement Date and Account Number. These elements are crucial for ensuring that payments are properly recorded against the correct account and period. Mismatches or typos can lead to misplaced payments or even charges of missing payments.

Underestimating the importance of the section detailing the Late Fee policy is another mistake. If payment is received after the specified date, a late fee is charged. Borrowers must be fully aware of this date and the potential financial consequences of missing it.

Errors in reporting the Outstanding Principal or Interest Rate can also occur. This section helps you understand the status of your loan and how your payments are allocated. Misinterpretation or incorrect entry here can lead to a misunderstanding of the loan's terms or your financial obligations.

One of the most consequential areas that is often mishandled is the explanation of the Amount Due. This includes not only the principal and interest but also any amounts due for escrow. Failure to correctly understand or report these can lead to underpayment, resulting in a possible default on the mortgage.

The Transaction Activity section, which records charges, payments, and any fees, is another critical area. Not reviewing this section for accuracy can lead to unnoticed errors, such as incorrect late fees or uncredited payments. It's essential to ensure all transactions are correctly recorded and accounted for.

A frequent oversight is not updating or misunderstanding the Past Payments Breakdown. This overview provides valuable insights into how your payments have been applied over time. Ignoring this section can lead to unawareness about the progress you've made on your loan, or misunderstanding the allocation towards principal, interest, escrow, and fees.

The instructions for the Amount Due at the bottom of the form also pose a challenge for many. This section, repeated for emphasis, includes critical payment instructions and the late fee warning. Neglecting to double-check this information can lead to incorrect payments.

Lastly, many overlook the Important Messages section, which includes vital notes about partial payments and delinquency notices. This oversight can limit a borrower's understanding of their rights and obligations, especially in challenging times or if they're already facing financial difficulties.

In sum, while filling out a Mortgage Statement form may seem straightforward, it’s fraught with potential pitfalls. Paying careful attention to each section, confirming all information is accurate and complete, and understanding the implications of each part of the statement can help avoid these common mistakes. It's always beneficial to review your form closely or seek clarification on any sections you do not fully understand.

Understanding the various documents and forms associated with your mortgage is essential for managing your home loan effectively. In addition to your Mortgage Statement, which outlines your current balance, interest rate, and recent transaction history, several other crucial documents play a significant role in ensuring you stay informed about your mortgage status. These documents work in tandem to provide a comprehensive overview of your mortgage details, payment history, and any actions required on your part.

Keeping these documents organized and understanding their content is crucial for effectively managing your mortgage. They serve as a roadmap to your financial obligations and provide essential information about the terms, conditions, and status of your loan. If you ever have questions about any of these documents or how they relate to your mortgage, speaking with a financial advisor or your loan servicer can provide clarity and guidance.

The Loan Estimate document shares similarities with the Mortgage Statement, especially in how it outlines the costs associated with a loan before its finalization. Like the Mortgage Statement, it provides details on the loan amount, interest rates, and monthly payments. However, the Loan Estimate is typically provided at the beginning of the loan application process, giving borrowers an overview of expected costs, while the Mortgage Statement gives an ongoing account of the loan's status, including principal, interest, escrow for taxes and insurance, and any fees charged.

An Amortization Schedule also parallels the Mortgage Statement by detailing the breakdown of each payment throughout the life of the loan. It shows how much of each payment is applied toward the principal versus the interest, as well as the remaining balance after each payment. While the Amortization Schedule provides a long-term view of the loan's repayment, the Mortgage Statement focuses on the current status, including the most recent payment period, current balance, and upcoming due amount.

The Annual Escrow Statement, similar to a section of the Mortgage Statement, details the activity in the escrow account, including taxes and insurance paid out, as well as the adjustments made to the escrow payments for the coming year based on changes in tax or insurance costs. Both documents provide critical information about the parts of a mortgage payment that go towards escrow, but the Mortgage Statement offers a monthly snapshot, whereas the Annual Escrow Statement gives a yearly overview.

An Account Statement from a bank is akin to the Mortgage Statement but for a different product type. Bank Account Statements summarize the transactions that occurred within a specific period, including deposits, withdrawals, fees charged, and the ending balance. Similarly, the Mortgage Statement summarizes transactions related to the mortgage, like payments made, fees charged, and the remaining loan balance, offering a periodic financial status for both bank accounts and mortgages.

The Credit Card Statement shares functionality with the Mortgage Statement in providing a detailed log of account activity over a statement period. It lists purchases, payments, fees, and interest charges, alongside the total amount due by a certain date. While the Credit Card Statement deals with revolving credit and the Mortgage Statement with installment credit, both serve the crucial role of informing consumers about their account status, due amounts, and deadlines for payment.

The Notice of Default is a legal document that serves as a formal warning to borrowers that their mortgage payments are significantly overdue. While it does not provide a regular account summary like a Mortgage Statement, it offers crucial information on payment delinquencies, similar to the delinquency notice portion of the Mortgage Statement. Both documents alert borrowers to the seriousness of their payment situation, though the Mortgage Statement also includes comprehensive transaction and payment history in addition to delinquency notices.

When filling out the Mortgage Statement form, it is crucial to handle the document with care and accuracy. To ensure the statement is completed correctly and to avoid any unnecessary complications, here is a guide on what you should and shouldn't do:

By adhering to these guidelines, you can ensure the Mortgage Statement form is filled out comprehensively and correctly, ultimately aiding in the management of your mortgage in the most effective manner possible.

Understanding the Mortgage Statement form is crucial for homeowners, yet there are several misconceptions that can lead to confusion. Below is a clarification of some common misunderstandings:

Only the current payment is detailed: Many believe the Mortgage Statement only shows the amount due for the current month. In reality, this document provides a comprehensive breakdown, including the principal, interest, escrow amounts for taxes and insurance, fees charged, and the total amount due. It also includes a transaction activity section detailing charges and payments within a certain period.

A late fee is immediately applied after the due date: It's widely misunderstood that late fees are instantly applied after the payment due date. However, the statement specifies that the late fee is charged only if the payment is received after a certain date, allowing a grace period for borrowers.

All payments go directly to the principal and interest: One common misconception is that all payments made are immediately applied to reduce the principal and interest. The statement clearly shows that payments are also allocated towards escrow for taxes and insurance, and fees, alongside the principal and interest.

Prepayment penalties always apply: There's a belief that making additional payments towards the mortgage always incurs prepayment penalties. The Mortgage Statement indicates whether a prepayment penalty is applicable or not, providing borrowers with the necessary information to make informed decisions about extra payments.

Partial payments reduce the loan balance: Many think that any partial payment made towards the mortgage will decrease their loan balance. However, the Mortgage Statement clarifies that partial payments are held in a suspense account and not applied to the mortgage until the balance of a partial payment is paid, at which point it will be applied to the loan.

Escrow amounts are fixed: Another common misconception is that the escrow amount for taxes and insurance is a fixed figure. The Mortgage Statement includes an escrow amount that can fluctuate based on changes in taxes or insurance premiums, ensuring that homeowners have an accurate account of funds required for these expenses.

By addressing these misconceptions, homeowners can better understand their Mortgage Statement form, empowering them to manage their mortgage payments more effectively.

Filling out and using the Mortgage Statement form correctly is crucial to managing your loan effectively. Here are six key takeaways:

By being mindful of these key points, you can better manage your mortgage and avoid potential issues that might arise from misunderstandings or mismanagement of your loan. Always reach out to your loan servicer if you have questions about your statement or your loan in general.

California Odometer Disclosure Statement Pdf - An official record of a vehicle's mileage, confirmed and notarized by a public official.

Certificate of Membership - Record, organize, and manage your company's membership interests efficiently with this laid-out ledger form.

Fedex Delivery Manager - Allows for contactless delivery by FedEx at an agreed-upon location at your home.