Fill Out Your IRS W-3 Template

Fill Out Your IRS W-3 Template

Every year, businesses across the United States gear up for the crucial task of reporting their employees' wage and tax statements through the Internal Revenue Service (IRS) W-3 form. This essential document, acting as a summary of individual W-2 forms, provides a comprehensive overview of the total earnings, Social Security wages, Medicare wages, and tax withholdings for all employees within a given tax year. Its accuracy is paramount, not just for staying compliant with federal tax laws, but also for ensuring that employees' Social Security and Medicare benefits are correctly reported and calculated. Employers must navigate through the details of the W-3 form diligently, understanding its significance in the tax filing process and the critical deadlines to avoid potential penalties. By ensuring the precise reporting of wages and taxes, businesses play a crucial role in maintaining the integrity of the tax system and supporting the financial welfare of their workforce.

Attention:

You may file Forms

The maximum amount of dependent care assistance benefits excludable from income may be increased for 2021. The American Rescue Plan Act of 2021 permits employers to increase the amount of dependent care benefits under their plans that can be excluded from an employee’s income from $5,000 ($2,500 for married filing separately) to up to $10,500 ($5,250 for married filing separately). See section C of Notice

Internal Revenue Bulletin:

Note: Copy A of this form is provided for informational purposes only. Copy A appears in red, similar to the official IRS form. The official printed version of this IRS form is scannable, but the online version of it, printed from this website, is not. Do not print and file Copy A downloaded from this website with the SSA; a penalty may be imposed for filing forms that can’t be scanned. See the penalties section in the current General Instructions for Forms

Please note that Copy B and other copies of this form, which appear in black, may be downloaded, filled in, and printed and used to satisfy the requirement to provide the information to the recipient.

To order official IRS information returns such as Forms

See IRS Publications 1141, 1167, and 1179 for more information about printing these tax forms.

DO NOT STAPLE

33333

b

Kind of Payer

(Check one)

a Control number |

|

|

For Official Use Only ▶ |

||

|

|

|

|

|

OMB No. |

|

941 |

Military |

943 |

|

944 |

▲ |

|

||||

|

|

|

|

Kind |

|

|

|

Hshld. |

Medicare |

of |

|

|

Employer |

||||

|

emp. |

govt. emp. |

|||

|

|

|

|

|

(Check one) |

▲

None apply |

501c |

|||||||||

|

|

|

|

|

|

|

|

sick pay |

||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

(Check if |

||

State/local |

State/local 501c Federal govt. |

|||||||||

applicable) |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

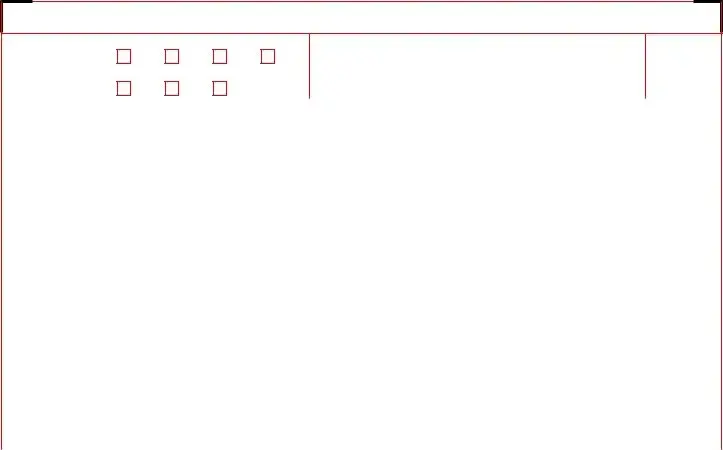

c Total number of Forms |

|

d Establishment number |

1 Wages, tips, other compensation |

2 Federal income tax withheld |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

e Employer identification number (EIN) |

3 Social security wages |

4 Social security tax withheld |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f Employer’s name |

|

5 |

Medicare wages and tips |

6 Medicare tax withheld |

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Social security tips |

8 Allocated tips |

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

|

|

10 Dependent care benefits |

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

11 Nonqualified plans |

12a Deferred compensation |

|

||||

|

g Employer’s address and ZIP code |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

|

h Other EIN used this year |

|

13 For |

12b |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|||||

|

15 State |

Employer’s state ID number |

14 Income tax withheld by payer of |

|

||||||||

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 State wages, tips, etc. |

|

17 State income tax |

18 Local wages, tips, etc. |

19 Local income tax |

|

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

Employer’s contact person |

|

|

Employer’s telephone number |

For Official Use Only |

|

||||||

|

|

|

|

|

|

|

|

|

|

|||

|

Employer’s fax number |

|

|

Employer’s email address |

|

|

|

|

||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return and accompanying documents, and, to the best of my knowledge and belief, they are true, correct, and complete.

Signature ▶ |

Title ▶ |

|

Date ▶ |

Form |

2022 |

Department of the Treasury |

|

Internal Revenue Service |

|||

Send this entire page with the entire Copy A page of Form(s)

Do not send any payment (cash, checks, money orders, etc.) with Forms

Reminder

Separate instructions. See the 2022 General Instructions for Forms

Purpose of Form

Complete a Form

The SSA strongly suggests employers report Form

•

•File Upload. Upload wage files to the SSA you have created using payroll or tax software that formats the files according to the SSA’s Specifications for Filing Forms

When To File Paper Forms

Mail Form

Where To File Paper Forms

Send this entire page with the entire Copy A page of Form(s)

Social Security Administration

Direct Operations Center

Note: If you use “Certified Mail” to file, change the ZIP code to

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions.

Cat. No. 10159Y

| Fact Name | Description |

|---|---|

| Purpose | The IRS W-3 form serves as a summary of an employer's total annual wages paid and taxes withheld from employees' paychecks. |

| Requirement | It is required by the IRS for employers to file a W-3 form alongside W-2 forms for all their employees annually. |

| Deadline | The W-3 must be filed with the Social Security Administration (SSA) by January 31st following the reporting year. |

| Electronic Filing | Employers can file the W-3 form electronically through the SSA's Business Services Online (BSO) or by mail. |

| State-Specific Forms | Some states require a separate state-specific form, governed by the individual state's department of revenue or taxation. |

| Penalties | Failure to file a W-3 form or filing late can result in penalties, which vary based on the delay and the size of the employer. |

Filling out the IRS W-3 form, also known as the Transmittal of Wage and Tax Statements, is a critical step for employers at the end of the tax year. This form is used to summarize the information of all W-2 forms, which report employee wages and taxes withheld, sent to the Social Security Administration (SSA). Accuracy and attention to detail are essential when completing this form to ensure compliance and timely processing of your tax documents. Here are the steps you need to follow to accurately fill out the IRS W-3 form.

Completing the IRS W-3 form is a straightforward process when approached with organization and attention to detail. By following the steps outlined above, employers can fulfill their tax reporting obligations accurately and efficiently, helping to ensure that employee wage and tax information is correctly reported to the SSA.

The W-3 form, officially known as the Transmittal of Wage and Tax Statements, is a summary document that the Internal Revenue Service (IRS) requires. Employers must submit this form to report the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the previous year. It accompanies the W-2 forms, which are sent to each employee and the Social Security Administration (SSA).

Any employer required to file W-2 forms for employees must also file the W-3 form. It's a way to report the total of all W-2s and confirm the information sent to the Social Security Administration is accurate.

The W-3 form is usually due by January 31 each year, the same deadline as the W-2 forms. This means that by January 31, the form, along with copies of all the W-2s for the previous tax year, should be sent to the Social Security Administration.

Employers can file a W-3 form either electronically or on paper. Electronic filing is preferred by the IRS and is required for employers who issue 250 or more W-2 forms. You can use the SSA’s Business Services Online (BSO) to submit W-2s and W-3 forms electronically. If filing on paper, you must use the official, scanner-readable form rather than a printout.

The W-3 form includes total amounts from the W-2 forms, such as:

It essentially summarizes the total compensation paid to employees and taxes withheld.

Filing the W-3 form late can result in penalties. The amount depends on how late the form is filed and the size of your business. Penalties can range from $50 per W-2 if you file within 30 days past the due date, to a maximum of $270 per W-2 if filed after August 1 or not at all.

No, self-employed individuals do not need to file a W-3 form. This form is only for employers reporting income and withholdings for their employees. Self-employed individuals typically report their income and expenses on a Schedule C form and may have other filing requirements.

Yes, if you discover an error on a W-3 after submitting it, you can correct it. To do this, you'll need to fill out a Form W-2c (Corrected Wage and Tax Statement) for each employee affected by the error and a Form W-3c (Transmittal of Corrected Wage and Tax Statements) to summarize the corrected W-2c forms. These corrected forms should be filed as soon as possible to minimize potential penalties.

Filling out the IRS W-3 form, which summarizes the total earnings, tax withholdings, and other payroll information for all employees for a business, is a critical annual task for employers. However, it is common for mistakes to be made during this process, leading to potential headaches and issues with the Internal Revenue Service (IRS). Here are nine common errors employers should be vigilant about.

One widespread mistake is not double-checking the Social Security numbers. This might seem like a simple oversight, but inaccuracies here can lead to significant problems with employee records and potential mismatch notices from the Social Security Administration (SSA).

Another common error is failing to report all employee compensation. This includes not only wages but also other forms of compensation such as bonuses, commissions, and fringe benefits. Omitting any form of compensation can result in an understatement of tax liabilities.

Employers often neglect the importance of accurately reporting state and local taxes. With the varying rates and rules across jurisdictions, it's crucial to report these figures correctly to avoid issues with state and local tax authorities.

Miscalculating withholding amounts is another error that frequently occurs. Whether it's federal income tax, Social Security, or Medicare tax, accurate calculation is essential. Miscalculations can lead to either underpayment or overpayment of taxes.

A significant mistake made by employers is submitting the form late. The IRS has strict deadlines for when the W-3 form must be filed, and failing to meet these deadlines can result in penalties and interest charges.

Some businesses mistakenly use the wrong tax year on the form. This error can cause a lot of confusion and necessitate the resubmission of the form with the correct year, leading to unnecessary delays and complications with employee records.

An error that can lead to processing delays or rejections is not using the correct version of the form. The IRS updates its forms regularly, and using an outdated version can lead to inaccuracies in submitted information.

Another frequent misstep is poor handwriting or illegibility when filling out the form manually. This can result in incorrect data processing or the need for clarification, delaying the entire process.

Lastly, an often-overlooked error is not retaining a copy for business records. Employers must keep a copy of the W-3 form for at least four years, as the IRS may request it for future reference. Failure to do so could pose problems if discrepancies need to be resolved in later years.

By being aware of and avoiding these common mistakes, employers can ensure their IRS W-3 filings are accurate and compliant, thus avoiding unnecessary penalties and ensuring their employees' records are correctly maintained.

When businesses prepare their wage reports for the IRS, form W-3, "Transmittal of Wage and Tax Statements," is a crucial document. However, it's often not the only document needed during this process. Several other forms and documents commonly accompany the IRS W-3 form to ensure compliance and accurate reporting to the Internal Revenue Service. Below is an overview of four such documents that are frequently used in conjunction with the W-3 form.

Together with Form W-3, these documents form a comprehensive suite of tax reporting tools that facilitate accurate and compliant reporting of employee wages, taxes withheld, and unemployment liabilities. Understanding each document's purpose and how they interlink can greatly simplify the tax reporting process for employers.

The IRS W-3 form, crucial for summarizing the total earnings, Social Security wages, Medicare wages, and withholding for all employees in a year, bears resemblance to the IRS W-2 form. Employers use the W-2 form to report individual employee wages and the taxes withheld from their paychecks. Each employee's financial information on the W-2 form is compiled to fill out the W-3 form. Thus, the W-3 serves as a transmittal document for all the W-2 forms an employer submits to the Social Security Administration.

Another document similar to the IRS W-3 form is the Form 1096. This form functions as an annual summary and transmittal document for all types of Form 1099, which reports various kinds of non-employee compensation and financial transactions to the IRS. Like the W-3 form compiles W-2 information for employees, the Form 1096 collates information from multiple 1099 forms, serving as a cover sheet when submitting paper copies of the 1099s to the IRS.

Form 941 is also akin to the IRS W-3 form in its function as a summary document, but it focuses on reporting quarterly Federal tax returns. Employers use this form to report income taxes, Social Security tax, or Medicare tax withheld from employees' paychecks and to pay the employer's portion of Social Security or Medicare tax. While the W-3 summarizes annual wage information and the related withholdings for all employees, Form 941 serves a similar purpose on a quarterly basis.

Lastly, the Form W-3SS is related specifically to employers in the U.S. territories like the Northern Mariana Islands, Guam, American Samoa, and the U.S. Virgin Islands. This form fulfills a role similar to the continental W-3 form by summarizing total wages, tax withholdings, and Social Security and Medicare contributions for employees. The distinction is that W-3SS is tailored to the Social Security and Medicare reporting requirements for employers operating within U.S. territories.

Filling out the IRS W-3 form, a crucial document for reporting total yearly wages and taxes withheld from employees' paychecks, requires careful attention to detail. To ensure accuracy and compliance, here are vital dos and don'ts to keep in mind:

Adhering to these guidelines can help streamline the process, ensuring that the necessary tax information is accurately and efficiently reported to the IRS. Always take the time to review the IRS instructions for the W-3 form each tax year, as requirements and recommendations can evolve.

When it comes to understanding IRS forms, it's easy to get tangled up in misconceptions, especially with forms like the W-3. The W-3 form, known as the Transmittal of Wage and Tax Statements, often confuses many. Let's clear up some of the common misunderstandings:

Understanding the correct procedures and requirements for filing a W-3 form can save businesses time and avoid fines. Always make sure to double-check your forms for accuracy and submit them on time.

The IRS W-3 form, known as the Transmittal of Wage and Tax Statements, plays a crucial role in annual tax reporting for employers. Understanding its purpose, deadlines, and requirements is essential to ensure compliance and avoid penalties. Here are eight key takeaways:

Comprehending these key points about the IRS W-3 form will help employers navigate the complexities of tax reporting with greater ease and accuracy, thus fulfilling their obligations while safeguarding their employees' information.

Melaleuca Membership Cost - Ensures a seamless experience for customers looking to temporarily stop their Preferred Customer benefits with Melaleuca.

Ncnda Template - Includes clauses to safeguard against the avoidance of fee payments among known introductions.

Imm 5707 E - Accuracy on the IMM5707 is crucial as it impacts future immigration applications and the verification of family details.