Fill Out Your IRS Schedule B 941 Template

Fill Out Your IRS Schedule B 941 Template

Navigating the complexities of tax documentation is crucial for businesses in maintaining compliance with federal regulations. Among these documents, the IRS Schedule B 941 form stands out as a pivotal piece for employers who withhold taxes from employees' wages. This form acts as a companion to the primary Form 941, Employer's Quarterly Federal Tax Return, and is specifically designed for those who report taxes on a semi-weekly schedule. It plays an essential role by detailing the tax amounts that employers have deposited throughout the quarter and helps in pinpointing the exact timing of these deposits. Understanding the nuances of Schedule B is vital for businesses not only to adhere to the tax codes but also to avoid potential penalties associated with misreporting or late submissions. This form, while seemingly straightforward, requires meticulous attention to detail, as errors or inaccuracies can lead to complications with the IRS. Through a thorough breakdown of the major aspects of the IRS Schedule B 941 form, businesses can gain insight into its importance, how to accurately complete it, and the implications it carries for their tax reporting procedures.

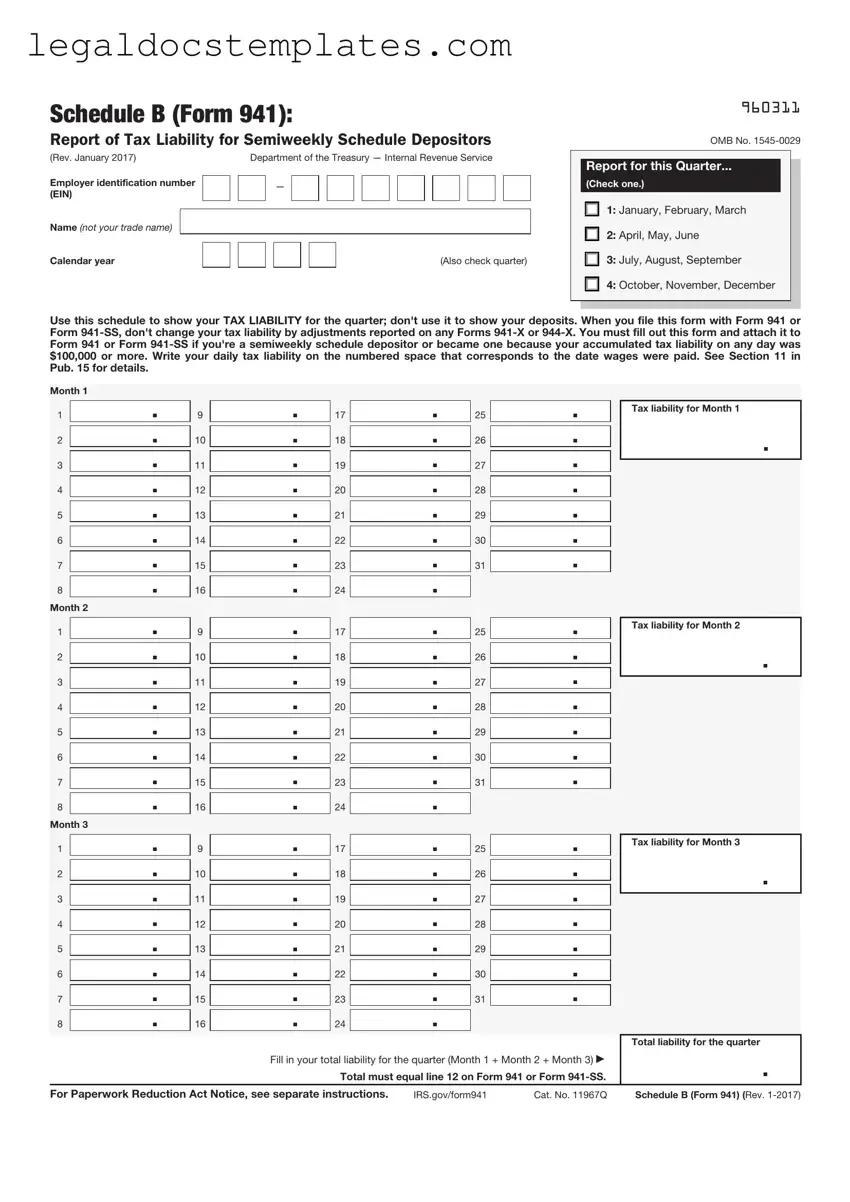

Schedule B (Form 941):

Report of Tax Liability for Semiweekly Schedule Depositors

(Rev. January 2017) |

|

|

Department of the Treasury — Internal Revenue Service |

|||||||||||||||||||

Employer identification number |

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Also check quarter) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

960311

OMB No.

Report for this Quarter...

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Use this schedule to show your TAX LIABILITY for the quarter; don't use it to show your deposits. When you file this form with Form 941 or Form

Month 1

1 .

.

2 .

.

3 .

.

4 .

.

5 .

.

6 .

.

7 .

.

8 .

.

Month 2

1 .

.

2 .

.

3 .

.

4 .

.

5 .

.

6 .

.

7 .

.

8 .

.

Month 3

9 .

.

10 .

.

11 .

.

12 .

.

13 .

.

14 .

.

15 .

.

16 .

.

9 .

.

10 .

.

11 .

.

12 .

.

13 .

.

14 .

.

15 .

.

16 .

.

17 .

.

18 .

.

19 .

.

20 .

.

21 .

.

22 .

.

23 .

.

24 .

.

17 .

.

18 .

.

19 .

.

20 .

.

21 .

.

22 .

.

23 .

.

24 .

.

25 .

.

26 .

.

27 .

.

28 .

.

29 .

.

30 .

.

31 .

.

25 .

.

26 .

.

27 .

.

28 .

.

29 .

.

30 .

.

31 .

.

Tax liability for Month 1

.

Tax liability for Month 2

.

1 |

|

. |

9 |

|

. |

17 |

|

|

. |

25 |

|

. |

|

Tax liability for Month 3 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

18 |

|

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

19 |

|

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

20 |

|

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

21 |

|

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

22 |

|

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

23 |

|

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

24 |

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liability for the quarter |

|

|

|

|

Fill in your total liability for the quarter (Month 1 + Month 2 + Month 3) |

. |

|||||||||

|

|

|

|

|

|

Total must equal line 12 on Form 941 or Form |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see separate instructions. |

IRS.gov/form941 |

Cat. No. 11967Q |

Schedule B (Form 941) (Rev. |

|||||||||||

| Fact Name | Description |

|---|---|

| Purpose of Form | The IRS Schedule B (Form 941) is used by employers to report tax liability for social security, Medicare, and withheld income taxes on a semi-weekly schedule or to report these taxes for the quarter if the employer is a seasonal employer, agricultural employer, or is otherwise not required to file Form 941 monthly. |

| Who Must File | Employers who have accumulated $50,000 or more in employment taxes in the lookback period, or those who have been notified by the IRS to file semi-weekly, must use Schedule B with their Form 941. Additionally, certain seasonal businesses, agricultural employers, and others exempt from monthly deposits must file this schedule to report quarterly liabilities. |

| Filing Schedule | Schedule B (Form 941) must be filed quarterly along with Form 941. The due dates for filing are the last day of the month following the end of a quarter, specifically April 30, July 31, October 31, and January 31 for the respective quarters. |

| Governing Law | Form 941 and its Schedule B are governed by the Internal Revenue Code (IRC) as federal laws and regulations, overseen by the Internal Revenue Service (IRS). There are no state-specific laws governing these forms since employment taxes are federally mandated. |

Filling out the IRS Schedule B (Form 941) is a critical task for employers who need to report their tax liability for social security, Medicare, and withheld income taxes on a semi-weekly schedule or those who accumulated a $100,000 tax liability on any given day during a reporting period. While the form might seem daunting at first, breaking down the process into manageable steps can make it more approachable. The key is to understand each section and what information is required. This step-by-step guide aims to simplify the process, ensuring that employers can complete the form accurately and comply with IRS requirements.

Steps for Filling Out the IRS Schedule B (941)

In summary, while filling out Schedule B (Form 941) may seem complex, following a step-by-step approach can help ensure accuracy and compliance. By carefully reporting each semi-weekly tax liability and totaling these amounts accurately, employers can fulfill their reporting obligations effectively. It's always advisable to double-check the form for any errors before submission and consult the IRS guidelines or a tax professional if any questions arise during the process.

The IRS Schedule B (Form 941) is a tax form required for businesses that report taxes on a semi-weekly schedule. This includes employers who withhold federal income tax, social security tax, or Medicare tax from their employees' paychecks or who must pay the employer's portion of social security or Medicare tax. If the total taxes after adjustments and credits are $50,000 or less in the lookback period, and you reported taxes for any quarter in the previous calendar year, you'll likely need to file this form.

Schedule B (Form 941) is filed quarterly, along with your Form 941, Employer's QUARTERLY Federal Tax Return. The due dates for filing are the last day of the month following the end of a quarter, which are April 30, July 31, October 31, and January 31.

To complete Schedule B, you'll need the following information:

Yes, you can file Schedule B (Form 941) electronically. The IRS encourages electronic filing because it's faster and reduces the risk of errors. You can file electronically through IRS-approved e-file providers or through your tax professional who uses e-file.

If you make a mistake on your Schedule B (Form 941), you should correct it as soon as possible to avoid potential penalties. You would typically use Form 941-X, Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund, to make corrections. It's important to carefully follow the instructions on Form 941-X to ensure your corrections are processed correctly. If you have questions or are unsure how to proceed, consulting with a tax professional can be very helpful.

One common mistake that individuals often make when filling out the IRS Schedule B (941), a form used for reporting taxes associated with employment, is the incorrect calculation of tax liability. This error usually stems from a misunderstanding or oversight of the tax rates and thresholds applicable to the reporting period. Given that tax rates and payroll thresholds can change from year to year, it is crucial to stay updated with the Internal Revenue Service’s (IRS) guidelines to ensure accurate calculations. Even a minor miscalculation can result in significant discrepancies, leading to potential penalties or additional scrutiny from the IRS.

Another frequent oversight involves the improper reporting of the tax liability period. The IRS Schedule B (941) requires taxpayers to report their liability according to the specific timeframe in which the wages were paid, not when the payroll taxes were withheld. This distinction is critical yet often overlooked, causing many to report their liabilities incorrectly. The precise reporting of the liability period plays a pivotal role in maintaining the correct tax records and ensuring compliance with IRS regulations.

Failing to sign and date the form constitutes a surprisingly common yet easily avoidable mistake. An unsigned or undated Schedule B (941) is deemed incomplete by the IRS and can lead to the rejection of the form. This seemingly minor oversight can have major implications, including delays in processing and potential penalties for late submission. It's essential to review the form thoroughly before submission to avoid such oversights, ensuring that all the required signatures and dates are present and correctly filled.

Underestimating the importance of accurate employer identification numbers (EINs) is another error often encountered on the IRS Schedule B (941). An incorrect EIN not only jeopardizes the proper attribution of tax payments but also can lead to confusion, unnecessary correspondence with the IRS, and processing delays. The EIN serves as a critical identifier for businesses in the eyes of the IRS, making its accurate reporting on all tax-related documents imperative for smooth processing and tracking of tax liabilities and payments.

When businesses navigate the complexities of tax reporting, particularly those related to payroll, the IRS Schedule B (Form 941) stands out as an essential document for employers who report payroll taxes on a semiweekly schedule. However, this form does not exist in isolation. Understanding and preparing several other forms and documents is crucial for comprehensive compliance and accurate tax reporting. Here’s a brief look at some of these key documents often used in conjunction with Schedule B (Form 941).

Together, these forms create a framework for detailed and compliant payroll tax reporting. Employers must stay informed about each document's purpose and requirements to ensure thorough and accurate tax reporting, thereby avoiding penalties and underpayments. As tax regulations and forms undergo continual updates, maintaining current knowledge and consulting with a tax professional when necessary are crucial steps in the tax preparation process. Employers should approach this task with diligence and attention to detail, securing their standing with tax authorities and ensuring the well-being of their workforce through proper tax practices.

The IRS Schedule B (Form 941) closely resembles the Form 940, which is the Employer's Annual Federal Unemployment (FUTA) Tax Return. Both forms serve as supplemental reports for businesses, designed to detail specific tax obligations to the IRS over the calendar year. Just like Schedule B breaks down an employer's federal tax liability per pay period, Form 940 outlines an employer’s annual contributions to federal unemployment taxes, providing a summary of what they owe or have paid throughout the year. This similarity lies in their function to categorize and summarize tax details tied to payroll obligations.

Another document akin to the IRS Schedule B (Form 941) is the Form W-2, Wage and Tax Statement. While the Schedule B focuses on an employer's detailed report of payroll taxes for each quarter, the W-2 form is given to each employee at the end of the year, detailing their annual wages and the amount of taxes withheld from their paycheck. Both documents are integral to tax reporting for employment, highlighting payroll taxes from two different perspectives: the employer's overall liability (Schedule B) and the individual employee’s deductions (W-2).

Form 945, Annual Return of Withheld Federal Income Tax, also shares similarities with Schedule B (Form 941) as they both involve tax withholding. Form 945 is used to report federal income tax withheld from nonpayroll items, such as pensions, annuities, and IRA distributions. Like Schedule B, which details payroll tax liabilities for each period, Form 945 provides a summary of withheld taxes on specified nonpayroll distributions. These forms work together to ensure the IRS has a comprehensive view of both payroll and nonpayroll withholding obligations fulfilled by an entity.

Finally, the Form 1099 series, particularly Form 1099-MISC (Miscellaneous Income), bears resemblance to Schedule B (Form 941) in its purpose to report specific financial activities to the IRS. Form 1099-MISC is used by businesses to report payments made to non-employees, such as independent contractors. Although Schedule B is focused on payroll tax liabilities and Form 1099-MISC on payments to non-employees, both are crucial for accurate tax reporting by businesses. They ensure that the IRS receives detailed information on different types of payments and liabilities accrued over the fiscal year.

The IRS Schedule B (941) form is an essential document for employers who report taxes. It is especially important for those who are required to deposit employment taxes on a semi-weekly schedule or that have accumulated $100,000 or more in taxes on any given day during a monthly or semi-weekly deposit period. Ensuring accuracy and completeness when filling out this form is crucial to prevent any potential issues with the IRS. Below are some key do's and don'ts to keep in mind during the process.

Do's:

Read the instructions provided by the IRS for Schedule B (941) carefully before you begin to fill out the form. This will help you understand the requirements and how to accurately report your tax liabilities.

Ensure that your Employer Identification Number (EIN), the name of your business, and the reporting period are correctly filled in, as these are critical for the IRS to match your form to your business records.

Report your tax liabilities by the specific dates as required. This is essential for semi-weekly depositors.

Use the correct tax period to avoid processing delays or notices from the IRS indicating discrepancies.

Double-check your calculations to ensure that the total tax liability reported on Schedule B (941) matches the liabilities reported on your Form 941.

Don'ts:

Don't leave any fields blank. If a certain section does not apply to your business, fill it with a "0" instead of leaving it empty.

Don't underestimate the importance of accuracy. Reporting incorrect amounts can lead to penalties or an audit.

Don't forget to sign and date the form. An unsigned form is considered incomplete and can lead to processing delays.

Don't ignore the IRS schedules and deadlines for filing. Late submissions can result in penalties.

Don't hesitate to seek professional advice if you are unsure about how to fill out the form or if you have specific questions related to your business situation. It's better to get it right with professional assistance than to make mistakes on your own.

Filling out the IRS Schedule B (941) form accurately and on time is crucial for employers. Following these guidelines can help ensure that the process is completed smoothly and correctly, avoiding unnecessary complications with tax filings.

The IRS Schedule B (Form 941) often finds itself shrouded in misconceptions. This form is essential for reporting tax liability for semi-weekly schedule depositors, and understanding it is crucial for compliance. Let’s dispel some common myths to clarify its purpose and requirements.

Understanding the IRS Schedule B (Form 941) and its requirements helps dispel fears and ensures businesses remain in compliance. Keeping these misconceptions in mind can guide semi-weekly depositors through the process more smoothly, avoiding common pitfalls along the way.

The IRS Schedule B (941) form is an essential document for employers who must report their taxes quarterly. It details the tax liability for each pay period, ensuring accuracy in reporting and payment of taxes withheld from employees. Understanding the intricacies of this form is crucial for compliance and avoiding penalties. Here are ten key takeaways:

When You Start a New Job, How Would You Sign Up for Direct Deposit? - Includes sections for both personal and banking information to ensure accurate deposit.

Tattoo Contract Template - The governing law and mandatory arbitration sections provide a predictable legal pathway for addressing any disputes, simplifying conflict resolution.

Dd 214 - The form provides a record of service including dates of active duty and total service time.