Fill Out Your Fl Dr 312 Template

Fill Out Your Fl Dr 312 Template

Understanding the FL DR 312 form, an affidavit of No Florida Estate Tax Due, is crucial for personal representatives managing an estate in Florida. This form plays a pivotal role when the estate is not liable for Florida estate tax and a federal estate tax return is not required. Specifically, it serves to affirm that the decedent's estate owes no Florida estate tax, per Chapter 198, F.S., and that a federal estate tax return, either federal Form 706 or 706-NA, need not be filed. The affidavit, effective from January 2021, also relieves the estate from the Department of Revenue's estate tax lien once properly filed with the clerk of the circuit court. Designed for those acting as personal representatives, who may be in actual or constructive possession of the decedent’s property, this form is admissible as evidence of non-liability for Florida estate tax. It replaces the need for the Florida Department of Revenue's Nontaxable Certificates for qualifying estates. Critical details such as the filing thresholds for federal estate tax returns and the procedural aspects of submitting the FL DR 312 form underscore its significance in estate administration. This comprehensive approach to delineating the use and requirements for the FL DR 312 affirms its importance in efficiently managing the responsibilities tied to the estates not subject to federal estate tax, thus streamlining the administrative process for personal representatives in Florida.

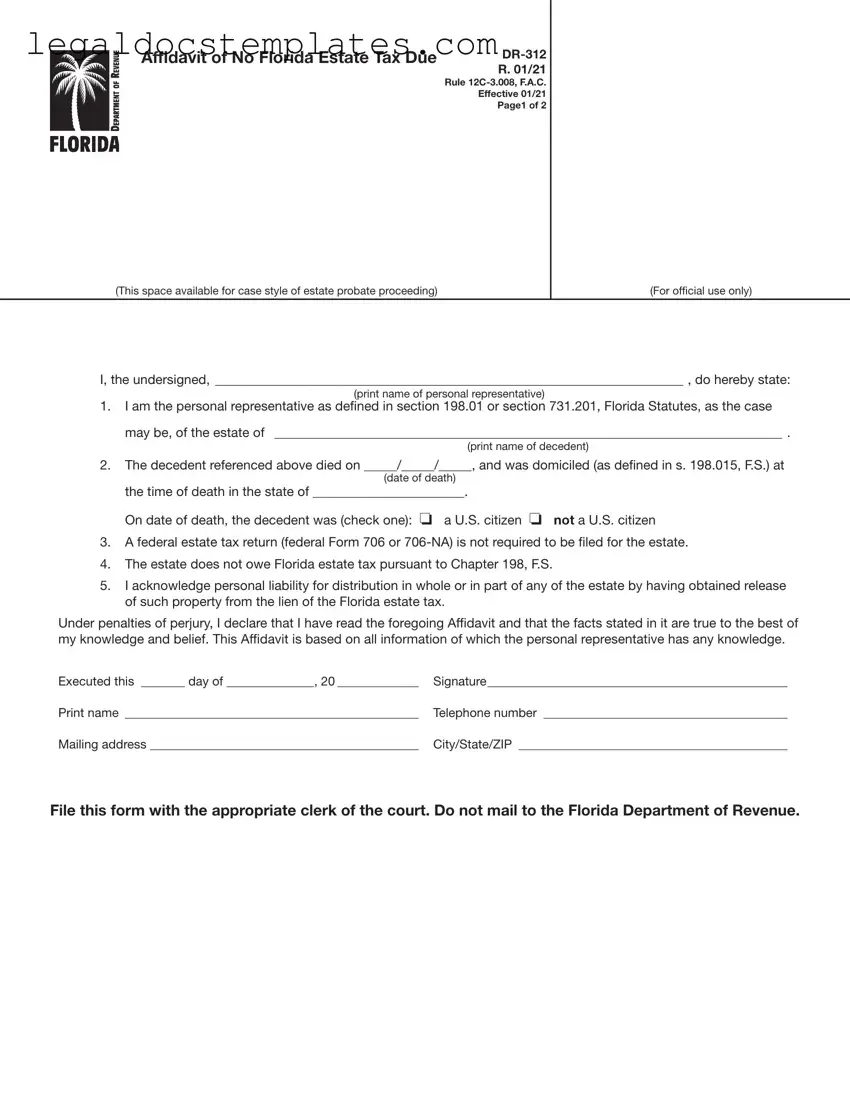

Affidavit of No Florida Estate Tax Due

Rule

Effective 01/21

Page1 of 2

(This space available for case style of estate probate proceeding) |

(For official use only) |

I, the undersigned, _______________________________________________________________________ , do hereby state:

(print name of personal representative)

1.I am the personal representative as defined in section 198.01 or section 731.201, Florida Statutes, as the case may be, of the estate of _____________________________________________________________________________ .

(print name of decedent)

2.The decedent referenced above died on _____/_____/_____, and was domiciled (as defined in s. 198.015, F.S.) at

(date of death)

the time of death in the state of _______________________.

On date of death, the decedent was (check one): o a U.S. citizen o not a U.S. citizen

3.A federal estate tax return (federal Form 706 or

4.The estate does not owe Florida estate tax pursuant to Chapter 198, F.S.

5.I acknowledge personal liability for distribution in whole or in part of any of the estate by having obtained release of such property from the lien of the Florida estate tax.

Under penalties of perjury, I declare that I have read the foregoing Affidavit and that the facts stated in it are true to the best of my knowledge and belief. This Affidavit is based on all information of which the personal representative has any knowledge.

Executed this _______ day of ______________, 20 _____________ |

Signature________________________________________________ |

Print name _______________________________________________ |

Telephone number _______________________________________ |

Mailing address ___________________________________________ |

City/State/ZIP ___________________________________________ |

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

R. 01/21

Page 2 of 2

Instructions for Completing Form

File this form with the appropriate clerk of the court. Do not mail to the Florida Department of Revenue.

General Information

If Florida estate tax is not due and a federal estate tax return (federal Form 706 or

Form

The

Where to File Form

Form

When to Use Form

Form

and a federal estate tax return (federal Form 706 or

Federal thresholds for filing federal Form 706 only: (For informational purposes only. Please confirm with Form 706 instructions.)

Date of Death |

Dollar Threshold |

(year) |

for Filing Form 706 |

|

(value of gross estate) |

|

|

2000 and 2001 |

$675,000 |

|

|

2002 and 2003 |

$1,000,000 |

|

|

2004 and 2005 |

$1,500,000 |

|

|

For 2006 and forward |

|

go to the IRS website at |

|

www.irs.gov to obtain |

|

thresholds. |

|

|

|

For thresholds for filing federal Form

If an administration proceeding is pending for an estate, Form

To Contact Us

Information, forms, and tutorials are available on the Department’s website floridarevenue.com

If you have any questions, or need assistance, call Taxpayer Services at

To find a taxpayer service center near you, go to: floridarevenue.com/taxes/servicecenters

For written replies to tax questions, write to: Taxpayer Services - Mail Stop

5050 W Tennessee St Tallahassee FL

Subscribe to Receive Email Alerts from the Department.

Subscribe to receive an email when Tax Information Publications and proposed rules are posted to the Department’s website. Subscribe today at floridarevenue.com/dor/subscribe.

Reference Material

Rule Chapter

| Fact | Description |

|---|---|

| Form Name and Number | Affidavit of No Florida Estate Tax Due DR-312 |

| Revision Date | 01/21 |

| Governing Law | Chapter 198, Florida Statutes, and Rule 12C-3.008, F.A.C. |

| Purpose | To declare that an estate owes no Florida estate tax and to remove the Department's estate tax lien. |

| Who Should File | Personal representatives of estates not subject to Florida estate tax and where a federal estate tax return (Form 706 or 706-NA) is not required. |

| Filing Location | With the clerk of the circuit court in the county where the decedent owned property. Not to be mailed to the Florida Department of Revenue. |

| Special Instructions | Must be recorded in public records of the county or counties where the decedent owned property. The 3-inch square in the upper right corner is for official use only. |

| Contact Information | Taxpayer Services at 850-488-6800 or floridarevenue.com for further information. |

Filing out the Form DR-312, Affidavit of No Florida Estate Tax Due, is an important step in managing the estate of a deceased individual in Florida under certain conditions. This form is specifically used when no federal estate tax return is required and the estate owes no Florida estate tax. By completing and filing this affidavit accurately, personal representatives can officially declare that the estate is exempt from these taxes, helping to expedite the handling of the decedent's estate. Here are the step-by-step instructions to fill out the form correctly, ensuring all legal requirements are met.

After successfully completing and filing the Form DR-312, the affidavit serves as evidence that the estate is not liable for Florida estate tax and effectively releases the estate from the Department of Revenue’s tax lien. Ensuring the form is accurately and promptly filed is crucial in the smooth administration of the decedent's estate. For further questions or assistance, consider reaching out to a legal professional or the Florida Department of Revenue.

The primary aim of the Florida DR-312 form, also known as the Affidavit of No Florida Estate Tax Due, is to formally declare that an estate is not liable for Florida estate taxes. This form is used by personal representatives or persons in actual or constructive possession of the decedent's property, as defined in Chapter 198, Florida Statutes. When no federal estate tax return is necessary and the estate owes no Florida estate tax, this affidavit serves as proof, thereby releasing the property from the Florida estate tax lien. Essentially, it enables the handling of estates with the assurance that Florida estate taxes are not a concern for the specific estate in question.

The DR-312 form should be utilized under two main conditions: first, if the estate does not meet the threshold for federal estate tax filing as stipulated by federal Form 706 or 706-NA guidelines; and second, when the estate owes no Florida estate tax under Chapter 198, Florida Statutes. It is particularly relevant for estates that are exempt from federal estate taxes based on the value thresholds, which have varied over the years according to IRS guidelines. Therefore, personal representatives managing estates that are not subject to these taxes should complete and file this affidavit.

The DR-312 form must be filed directly with the clerk of the circuit court in the county or counties where the decedent owned property. It is crucial not to mail this form to the Florida Department of Revenue, as it will not be processed by them. Instead, the completed form, properly attested to, should be recorded in the public records of the appropriate county, facilitating the release of any state tax liens on the estate's property.

To accurately fill out the DR-312 form, the personal representative needs to provide specific information, including:

For estate administration, the DR-312 form plays a critical role in evidencing that an estate is not subject to Florida estate taxes. Upon its proper filing and recording, the form acts as admissible proof to remove the Florida Department of Revenue's estate tax lien on the estate's property. This simplifies the estate administration process by clearly establishing the estate's tax status, which is fundamental for the distribution of assets and for closing the estate's administration proceedings in court.

Yes, the DR-312 form can be utilized for estates of non-U.S. citizens, provided the estate does not meet the requirements for filing a federal estate tax return (form 706-NA for nonresident alien decedents). The personal representative must check the appropriate box indicating the decedent's citizen status and ensure that all other criteria for not owing Florida or federal estate tax are met. This includes ensuring that the estate's value does not cross the thresholds that necessitate federal estate tax filing, which varies for nonresident aliens.

Filling out the FL DR 312 form, also known as the Affidavit of No Florida Estate Tax Due, is a critical step in the estate management process in Florida. However, errors can occur during this process, leading to potential legal complications or delays. Here are six common mistakes people make when completing this form.

One common mistake is the incomplete or incorrect identification of the personal representative. The form requires the personal representative to print their name clearly, identifying themselves as the individual responsible for the estate. It's crucial that this information matches the legal documents appointing them to this role. Any discrepancy can cause confusion or lead to the form being rejected by the court.

Another frequent error is the failure to accurately identify the decedent. The form requires the full legal name of the deceased, as well as their date of death and domicile state at the time of death. Mixing up these details or providing incomplete information can lead to serious issues in processing the affidavit, possibly affecting the estate's legal standing.

The form also asks whether a federal estate tax return is required, with responses based on the estate's value and specific thresholds. A mistake in understanding or acknowledging this requirement can lead to inaccuracies in the affidavit. If the estate's value necessitates a federal return, but the form erroneously states otherwise, the personal representative could face legal ramifications.

Often overlooked is the proper use of the space reserved for the clerk of the court. It is outlined that the 3-inch by 3-inch space in the upper right corner is exclusively for the clerk's use. Marking or writing in this area, even accidentally, can invalidate the form or at least necessitate its re-submission, leading to delays in the estate's processing.

A critical error made by many is the lack of acknowledgment regarding personal liability. By signing the form, the personal representative acknowledges their liability for any distribution of the estate that may contravene Florida's estate tax laws. Misunderstanding or overlooking this acknowledgment can lead to personal financial risk and legal issues if the estate is improperly distributed without fulfilling tax obligations.

Lastly, a common mistake is not properly filing the form with the appropriate clerk of the court. The DR-312 form is not to be mailed to the Florida Department of Revenue but rather recorded directly with the clerk of the circuit court in the county or counties where the decedent owned property. Failing to correctly file the form can lead to the estate remaining under a tax lien, potentially complicating property transfers and estate closure.

Avoiding these common mistakes requires attention to detail and a clear understanding of the form's instructions. By accurately completing and properly filing the FL DR 312 form, personal representatives can ensure a smoother process in affirming that no Florida estate tax is due, thus expediting the estate settlement process.

When managing the estate of a loved one, familiarizing oneself with the required forms and documents can pave the way for a smoother process. In addition to the Florida Form DR-312, an Affidavit of No Florida Estate Tax Due, several other forms often play crucial roles in the administration and closure of an estate. While the DR-312 serves as a declaration to the state that no Florida estate tax is owed by the estate, understanding the relevance and application of additional forms can further ensure compliance with state requirements and facilitate the estate's proceedings.

Each of these documents serves a specific purpose within the broader context of estate administration. By ensuring the proper preparation and submission of these forms, personal representatives can help guarantee that the estate is settled in accordance with Florida law and the wishes of the deceased. While the DR-312 is a key piece in affirming the estate's tax responsibilities, it's just one part of a larger procedural puzzle. Navigating through these requirements with care and diligence exemplifies a commitment to honoring one's responsibilities and the memory of the departed.

The Florida DR-312 form, serving as an affidavit to declare no Florida estate tax is due, shares similarities with several other estate-related documents across different jurisdictions. Among these, the California Form 1310 is a notable example. Much like the DR-312, Form 1310 is used to notify state tax authorities—in this case, the California Franchise Tax Board—about the deceased's tax affairs. Specifically, it's employed to claim a refund on behalf of a decedent, requiring information about the deceased and the claimant. Both forms serve as critical documents within the framework of estate settlement, ensuring proper notification to tax authorities and facilitating the resolution of the decedent's financial matters.

Another document akin to the DR-312 is the IRS Form 706 for the United States. This form is required for the estates of decedents to calculate and pay federal estate taxes where applicable. While the DR-312 confirms that no Florida estate tax nor federal estate tax Form 706 is due for Florida residents, Form 706 deals directly with the broader scope of federal estate taxation. Both documents underscore the necessity of addressing estate taxes but at different levels of governance—state for DR-312 and federal for Form 706, highlighting their roles in the compliance landscape for estates.

Similarly, in Texas, individuals may encounter the Texas Affidavit of Heirship, used to establish ownership of a decedent's property when there is no formal administration of the estate. While different in its primary function compared to the DR-312, the Texas Affidavit of Heirship shares the objective of simplifying estate settlement processes in the absence of a will. It provides a pathway for heirs to prove their right to inherit property without undergoing the full probate process, much as the DR-312 aims to streamline estate taxation matters by certifying no tax due.

Moreover, the New York ET-30 form bears resemblance to Florida's DR-312 in its purpose and application. The ET-30 is used when a New York resident's estate is not required to file a federal estate tax return and thus, is believed not to owe New York estate taxes. This form, like DR-312, is instrumental in estate planning and settlement, offering a means for executors or personal representatives to certify tax statuses. While each state has its unique tax laws and requisite forms, the DR-312 and ET-30 both play pivotal roles in affirming an estate's tax obligations—or lack thereof—to their respective state tax departments.

When filling out the Florida Department of Revenue Form DR-312, Affidavit of No Florida Estate Tax Due, it's important to follow the right steps and avoid common mistakes. Below are 10 key dos and don'ts to guide you through the process:

Adhering to these guidelines will help ensure the process goes smoothly and that the affidavit is properly completed and filed. This form plays a key role in the settlement of an estate by declaring that no Florida estate tax is due. Therefore, it's important to approach filling it out carefully and accurately.

Understanding the intricacies of legal forms and their implications can often lead to misconceptions, especially in the realm of estate management and tax obligations. The Florida Form DR-312, known as the Affidavit of No Florida Estate Tax Due, is no exception. This document has generated its share of misunderstandings, some of which can significantly impact the process of handling an estate. Here are five common misconceptions about this form and the truths behind them:

Dispelling these misconceptions is crucial for those navigating the complexities of estate management and taxation. A clear understanding of Form DR-312 ensures that personal representatives can accurately fulfill their duties while complying with Florida's tax laws.

Understanding the FL DR-312 form, also known as the Affidavit of No Florida Estate Tax Due, is essential for personal representatives managing the estate of a deceased person in Florida. Below are key takeaways to help navigate the process smoothly:

Properly completing and filing the FL DR-312 form is a critical step in managing the affairs of a decedent's estate in Florida. This ensures that the estate is processed correctly and efficiently, adhering to Florida's tax laws and regulations.

What Is Form W-3 - Errors on the W-3 form can lead to incorrect tax calculations and potential issues with employee Social Security credits.

Citizens Roof Certification Form - Reflecting best practices, this template offers a structured approach to roof certification, necessary for maintenance and sale proceedings.

Cash Receipt Generator - Enables businesses to give a professional and organized impression to customers and clients.