Printable Deed of Trust Template

Printable Deed of Trust Template

In the realm of real estate, secure transactions are paramount. The Deed of Trust form plays a pivotal role in this process, serving as a vital instrument for both lenders and borrowers. Essentially, it involves three parties: the borrower, the lender, and a trustee. This form is a type of secured real estate transaction that provides lenders with a level of safety concerning their investment. By transferring the property's title to a trustee, who holds it as security for the loan, the Deed of Trust ensures that the lender's interests are protected. Should a borrower fail to meet their obligations, the trustee has the authority to sell the property to recuperate the loan on behalf of the lender. This legal document not only outlines the responsibilities and rights of all involved parties but also stipulates the terms of the loan, including the payment schedule, interest rates, and the consequences of default. Understanding the Deed of Trust is crucial for anyone entering into a real estate transaction to ensure they are fully aware of the legal and financial implications.

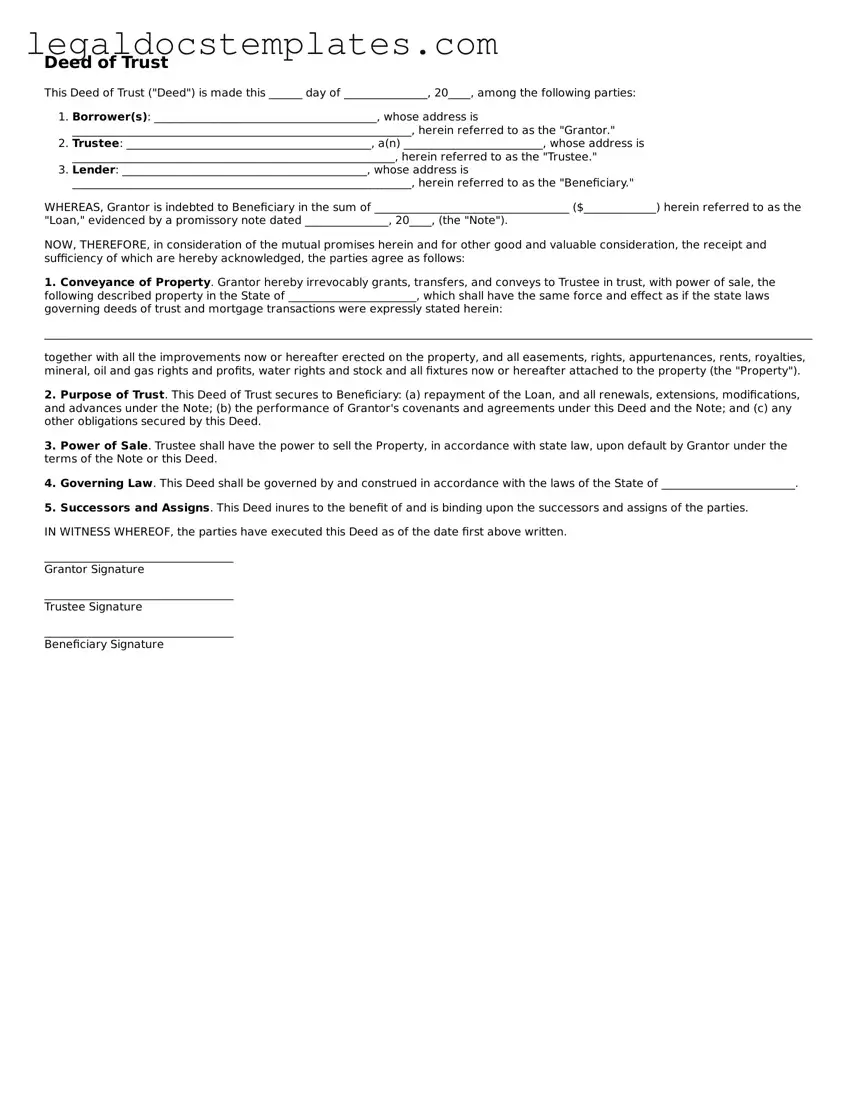

Deed of Trust

This Deed of Trust ("Deed") is made this ______ day of _______________, 20____, among the following parties:

WHEREAS, Grantor is indebted to Beneficiary in the sum of ___________________________________ ($_____________) herein referred to as the "Loan," evidenced by a promissory note dated _______________, 20____, (the "Note").

NOW, THEREFORE, in consideration of the mutual promises herein and for other good and valuable consideration, the receipt and sufficiency of which are hereby acknowledged, the parties agree as follows:

1. Conveyance of Property. Grantor hereby irrevocably grants, transfers, and conveys to Trustee in trust, with power of sale, the following described property in the State of _______________________, which shall have the same force and effect as if the state laws governing deeds of trust and mortgage transactions were expressly stated herein:

______________________________________________________________________________________________________________________________________________________________________________________________________

together with all the improvements now or hereafter erected on the property, and all easements, rights, appurtenances, rents, royalties, mineral, oil and gas rights and profits, water rights and stock and all fixtures now or hereafter attached to the property (the "Property").

2. Purpose of Trust. This Deed of Trust secures to Beneficiary: (a) repayment of the Loan, and all renewals, extensions, modifications, and advances under the Note; (b) the performance of Grantor's covenants and agreements under this Deed and the Note; and (c) any other obligations secured by this Deed.

3. Power of Sale. Trustee shall have the power to sell the Property, in accordance with state law, upon default by Grantor under the terms of the Note or this Deed.

4. Governing Law. This Deed shall be governed by and construed in accordance with the laws of the State of ________________________.

5. Successors and Assigns. This Deed inures to the benefit of and is binding upon the successors and assigns of the parties.

IN WITNESS WHEREOF, the parties have executed this Deed as of the date first above written.

__________________________________

Grantor Signature

__________________________________

Trustee Signature

__________________________________

Beneficiary Signature

| Fact Name | Description |

|---|---|

| Definition | A Deed of Trust is a document that secures a real estate transaction involving a loan by transferring legal title of a property to a trustee until the loan is paid off. |

| Parties Involved | Typically involves three parties: the borrower (trustor), the lender (beneficiary), and the trustee, who holds the property's title for the loan’s duration. |

| Function | Serves as a lien against the property, securing the repayment of the loan. |

| Governing Laws | Vary by state, but generally governed by state-specific real estate and contract law. |

| Foreclosure Process | Allows for a non-judicial foreclosure process in the event of default, meaning the property can be sold without court intervention, subject to state law. |

| Release of Deed | Once the loan is fully repaid, the trustee is required to issue a Deed of Reconveyance, releasing the lien and transferring the legal title back to the borrower. |

| State-Specific Forms | While the basic structure is similar, the specific requirements and forms can vary significantly from one state to another. |

| Usage | Primarily used in states where trust deeds are the standard method for securing a loan against real estate, including but not limited to California, Texas, and Virginia. |

Filling out a Deed of Trust form is a crucial step in the process of securing a mortgage or loan against a property. This document legally binds the borrower and the lender, ensuring that the property can be used as collateral for the loan. The process might seem daunting at first, but by following these outlined steps, you can complete the form accurately and efficiently. Remember, once this form is filled out and submitted, the next step will involve waiting for the processing and eventual approval from the lending institution. It's important to ensure all information is correct to avoid any delays.

After submitting the Deed of Trust form, it’s a matter of patience as the document goes through the necessary channels for processing and approval. Ensure that you keep a copy of the form for your records. This step is critical in the borrowing process as it legally secures the loan against the property. Taking the time to fill out this form correctly can save a significant amount of time and reduce the potential for legal complications down the line.

A Deed of Trust is a document that serves as proof of an agreement between a borrower and a lender, with a third party involved, known as the trustee. The borrower gives the trustee the legal title to the property as security for the loan provided by the lender. If the borrower repays the loan as agreed, the property title is transferred back to the borrower. If not, the trustee has the authority to sell the property to pay off the loan.

Although both are used to secure a loan on a property, a Deed of Trust involves three parties—the borrower, the lender, and the trustee—while a mortgage involves only two parties, the borrower and the lender. Unlike mortgages, where the legal system must process any foreclosure, with a Deed of Trust, the trustee can sell the property without court involvement if the borrower defaults on the loan.

The trustee is typically a neutral third party, such as a title company or a legal entity that holds the property's title until the loan is fully repaid. The trustee's main role is to facilitate the foreclosure process on behalf of the lender, if necessary, or release the lien on the property when the loan is paid off.

A Deed of Trust generally includes the following key elements:

No, not all states recognize a Deed of Trust as a means to secure a loan. Some states use Deeds of Trust, others use mortgages, and some allow both. It's essential to check the laws in the state where the property is located to understand which legal document is applicable.

A Deed of Trust is terminated when the borrower pays off the loan in full. Upon repayment, the trustee is responsible for recording a deed of reconveyance with the county recorder’s office, which indicates that the borrower's debt has been satisfied and transfers the property title back to the borrower free and clear of the lender's interest.

Yes, modifications can be made to a Deed of Trust, but all parties involved— the borrower, lender, and trustee—must agree to any changes. The modification must then be recorded with the appropriate government entity to be enforceable.

If a borrower defaults on a loan secured by a Deed of Trust, the trustee has the authority to foreclose on the property on behalf of the lender. This typically involves selling the property at a public auction. The process and rights involved vary by state, including any right the borrower may have to stop the foreclosure and reclaim the property by paying off the debt.

One common mistake when filling out a Deed of Trust form is not including all legal names correctly. Parties involved must provide their full, legal names to ensure that the document accurately reflects who is participating in the agreement. This is crucial for avoiding confusion or disputes regarding the property's title down the line. Using nicknames or shortened versions can lead to questions about the deed’s enforceability.

Another error often made is neglecting to provide a complete legal description of the property. A Deed of Trust requires a detailed legal description, which is more specific than just an address. This description typically includes lot numbers, block numbers, and subdivision names, as drawn from official records. Omitting this information can lead to disputes about what property is actually covered under the deed.

People sometimes fail to include the correct loan amount in the Deed of Trust. This document must reflect the exact amount of money being borrowed. Any inaccuracies in this area can complicate future dealings related to the loan, such as refinancing or repayment. It's imperative to double-check that the numbers are right before proceeding.

Errors in spelling, grammar, and punctuation are not uncommon and can be more than just embarrassing. They can actually affect the deed's clarity and legal standing. Attention to detail ensures that all information is understood as intended, thereby avoiding any potential legal ambiguities or misunderstandings.

Often overlooked is the requirement for all necessary parties to sign the document. This not only includes the borrower and lender but also any co-signers or guarantors. Without everyone’s signature, the Deed of Trust may not be legally binding. Ensuring that everyone signs the document in the presence of a notary also adds a layer of legal verification and protection.

Another frequent mishap is failing to attach any required legal schedules or appendices. If the Deed of Trust references additional documents, they must be attached and appropriately labeled. These appendices often contain crucial details that are integral to the deed's terms and conditions.

Not having the document notarized is a critical error. A Deed of Trust generally needs to be notarized to be recorded officially and considered valid. This step verifies the identity of the signers and affirms that they signed the document willingly and under no duress.

Submitting the deed without first reviewing it for accuracy and completeness is a mistake with potentially serious ramifications. This final check can catch any of the previously mentioned errors and others, like incorrect dates or missing pages. Once a deed is recorded, making changes becomes significantly more complicated.

Another common issue is miscalculating the fees associated with recording the deed. Each jurisdiction has its own fee structure for recording documents like a Deed of Trust. Underestimating or failing to pay these fees can delay the recording process, affecting the deed's legal standing.

Lastly, many people fail to obtain a copy of the recorded Deed of Trust. Once the document is officially recorded, obtaining a copy for personal records is crucial. This confirms the deed has been recorded and provides proof of the trust deed's conditions and responsibilities. It’s an essential step in maintaining transparency and accountability for all parties involved.

When it comes to securing a real estate transaction, particularly a mortgage, the Deed of Trust form plays a pivotal role. However, this document doesn't operate in isolation. Several other forms and documents are typically utilized alongside the Deed of Trust to ensure a comprehensive, secure, and legally sound transaction. Understanding these additional documents can help parties involved in real estate transactions navigate the process more smoothly and with a better grasp of their rights and obligations.

Navigating through the complexities of real estate transactions demands a thorough understanding of the documentation involved. The Deed of Trust is just one piece of the puzzle. By familiarizing oneself with the various forms and documents like the Promissory Note, Title Report, and others mentioned above, individuals can ensure they're fully prepared for the process. These documents collectively safeguard the interests of all parties involved, ensuring a clear and legally binding agreement is in place.

A Deed of Trust is similar to a mortgage, as both serve as security instruments used in securing a loan by using real estate as collateral. While a Deed of Trust involves three parties—the borrower, the lender, and a trustee—the mortgage typically involves only the borrower and the lender. The trustee in a Deed of Trust holds the legal title to the property on behalf of the lender and can facilitate the foreclosure process outside of court if necessary, unlike in a mortgage, where court action is usually required for foreclosure.

Comparable to a Promissory Note, a Deed of Trust also embodies an agreement related to borrowing money. However, while a Promissory Note details the borrower's promise to repay the loan, a Deed of Trust provides the legal framework for securing that loan with real property. This distinction makes the Deed of Trust not just a promise to pay but also offers a method for the lender to recoup their investment if the borrower fails to fulfill their repayment obligations.

Similar to a Warranty Deed, a Deed of Trust deals with the transfer of interest in real property. A Warranty Deed transfers ownership and guarantees that the seller holds clear title to the property, while a Deed of Trust does not transfer full ownership. Instead, it places a lien on the property as a security measure for a loan, with ownership interests being conditional on the loan's repayment.

A Grant Deed shares common ground with a Deed of Trust in that both involve the conveyance of real property rights. The Grant Deed transfers ownership from the seller to the buyer with a promise that the property hasn’t been sold to someone else. On the contrary, a Deed of Trust transfers a property interest as security for a loan, highlighting its role in financial transactions rather than outright ownership transfer.

The Mechanics Lien is another document that, like a Deed of Trust, creates a security interest in real property. However, a Mechanics Lien is specific to the construction industry, securing payment for workers and suppliers. In contrast, a Deed of Trust secures a loan used to purchase or refinance the property itself, signifying its broader application in real estate financing.

Similar to a Quitclaim Deed, a Deed of Trust involves documentation that impacts property titles. A Quitclaim Deed transfers any ownership interest the grantor may have without warranties, which is fairly limited compared to a Deed of Trust that places a lien on the property to secure a loan. The key difference lies in the specific rights transferred and the purpose of each document.

Comparable to an Assignment of Lease, a Deed of Trust involves the transfer of rights related to real property. An Assignment of Lease allows a tenant to transfer their leasehold interest to another party, whereas a Deed of Trust transfers the borrower's property interest to a trustee as collateral for a loan. Both documents involve the transfer of specific rights for distinct purposes.

A lien release is akin to a Deed of Trust in the sense that it is involved in the lien process on a property. However, while a Deed of Trust is used to place a lien, a lien release is used to remove one, indicating that the debt securing the property has been paid. The relationship between these two documents is inherently connected to the lifecycle of a loan secured by real estate.

Similarly, a Foreclosure Notice has a connection to a Deed of Trust, both being part of the foreclosure process. A Deed of Trust may contain provisions for a non-judicial foreclosure, allowing a trustee to sell the property if the borrower defaults. In contrast, a Foreclosure Notice is a formal notification that the foreclosure process has been initiated, marking a subsequent step in enforcing the security interest outlined in a Deed of Trust.

Lastly, a Power of Attorney (POA) document, while used in various contexts, relates to a Deed of Trust through its potential to grant someone the authority to handle real estate transactions, including those involving a Deed of Trust. For instance, a POA might authorize an individual to execute a Deed of Trust on behalf of another, demonstrating how both documents can play roles in managing real property interests, albeit for different purposes.

When filling out a Deed of Trust form, ensuring accuracy and thoroughness is crucial for the document's legality and validity. Below are essential guidelines to follow:

Do:

Don't:

The Deed of Trust is a document that plays a pivotal role in real estate transactions, specifically when it comes to securing a mortgage. However, there are several misconceptions surrounding this crucial document that can lead to confusion for individuals going through the home buying or selling process. It’s important to clarify these misunderstandings to ensure a smoother, more informed transaction.

A Deed of Trust and a Mortgage are the same. This is a common misconception. Although both serve as security for loans on real property, the structures differ. A Deed of Trust involves three parties: the borrower (trustor), the lender (beneficiary), and a neutral third party (trustee) who holds the title until the loan is repaid. A mortgage involves only two parties: the borrower and the lender.

Signing a Deed of Trust means you immediately transfer ownership of your property to the lender. This is not accurate. While the Deed of Trust does involve the transfer of the property's legal title to the trustee, the equitable title - the right to obtain full ownership - remains with the borrower as long as they adhere to the terms of the loan agreement.

Once a Deed of Trust is signed, the borrower no longer has any control over the property. This statement is misleading. The borrower retains significant control and use of the property during the term of the loan. The trustee holds the legal title purely for security purposes, and as long as the borrower complies with the terms of the Deed of Trust, including making timely payments, they maintain control over the property.

Deeds of Trust are only used in a few states. While it’s true that the use of Deeds of Trust is not uniform across all states, they are quite common. Many states allow for the use of both Deeds of Trust and mortgages, with the choice depending on the lender’s preference, the borrower’s situation, and specific state laws. The use of a Deed of Trust is not limited to a small number of states but is instead a widely utilized instrument in real estate financing.

Understanding these aspects of a Deed of Trust can help individuals navigate the complexities of real estate transactions with more confidence and peace of mind. It’s essential to have clear, accurate information to avoid misconceptions that could affect the decision-making process.

When filling out and using a Deed of Trust form, it's crucial to understand its purpose and ensure accuracy in its completion. Below are key takeaways to help guide you through this process:

Adhering to these takeaways can smooth the process of filling out and using your Deed of Trust form, making it a secure and effective tool for all parties involved.

Printable Lady Bird Deed Florida Form - As a part of comprehensive estate planning, the Lady Bird Deed can serve as a cornerstone for real estate transfer strategies.