Fill Out Your Cg 20 10 07 04 Liability Endorsement Template

Fill Out Your Cg 20 10 07 04 Liability Endorsement Template

In the realm of Commercial General Liability (CGL) insurance, navigating the waters of policy endorsements can be tricky, yet it’s essential for ensuring that coverage is tailored to meet specific needs. The CG 20 10 07 04 Liability Endorsement form is a critical document in this landscape, particularly for owners, lessees, or contractors who might find themselves as additional insureds under a policy. This particular form modifies the existing insurance policy by extending coverage to additional insured persons or organizations, identifying the nature of the coverage as it relates to "bodily injury," "property damage," or "personal and advertising injury" that arises from the direct or indirect actions of the named insured. What makes this endorsement stand out is its specificity in defining the circumstances under which the additional insured is covered, especially focusing on the legal and contractual boundaries that dictate the extent of the protection provided. Moreover, it introduces exclusions and limitations that directly impact the scope of coverage, especially emphasizing the conditions under which coverage ceases. Another critical aspect is the stipulation regarding the limits of insurance, which clarifies that the endorsement does not extend the policy's overall limits for the additional insured, but rather, adheres to the terms outlined within the contractual agreement or the existing insurance limits, whichever is lesser. Such measures ensure that the endorsement provides necessary coverage without overextending the policy's intent or the insurer's liability.

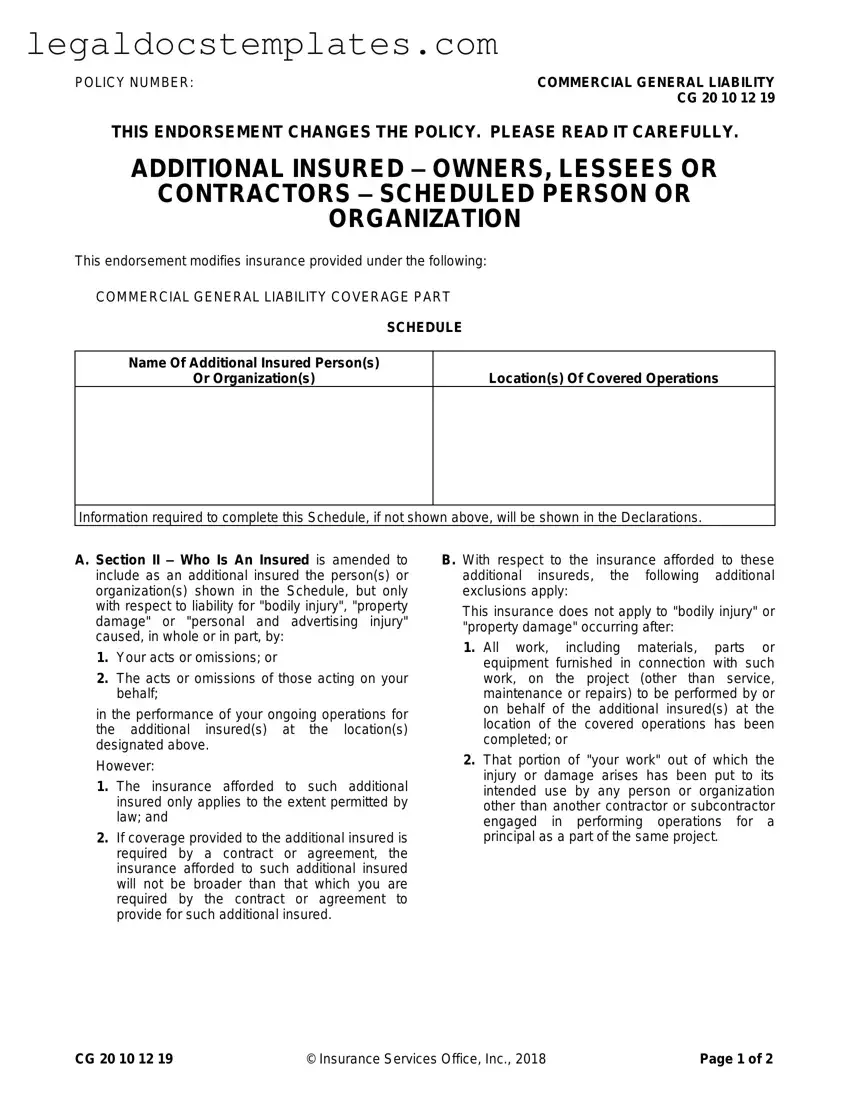

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 10 12 19 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR

CONTRACTORS – SCHEDULED PERSON OR

ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location(s) Of Covered Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by:

1.Your acts or omissions; or

2.The acts or omissions of those acting on your behalf;

in the performance of your ongoing operations for the additional insured(s) at the location(s) designated above.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following additional exclusions apply:

This insurance does not apply to "bodily injury" or "property damage" occurring after:

1.All work, including materials, parts or equipment furnished in connection with such work, on the project (other than service, maintenance or repairs) to be performed by or on behalf of the additional insured(s) at the location of the covered operations has been completed; or

2.That portion of "your work" out of which the injury or damage arises has been put to its intended use by any person or organization other than another contractor or subcontractor engaged in performing operations for a principal as a part of the same project.

CG 20 10 12 19 |

© Insurance Services Office, Inc., 2018 |

Page 1 of 2 |

C. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable limits of insurance;

whichever is less.

This endorsement shall not increase the applicable limits of insurance.

Page 2 of 2 |

© Insurance Services Office, Inc., 2018 |

CG 20 10 12 19 |

| Fact Name | Detail |

|---|---|

| Form Identification | The form is identified as CG 20 10 12 19, which is a Commercial General Liability Endorsement form issued by the Insurance Services Office, Inc., in 2018. |

| Purpose of the Form | This endorsement serves the purpose of adding certain person(s) or organization(s) as additional insureds under the commercial general liability coverage, specifically for liability arising from the named insured's operations for the additional insured(s). |

| Scope of Coverage | The coverage is extended to the additional insured(s) only with respect to liability for bodily injury, property damage, or personal and advertising injury caused, in whole or in part, by the named insured's acts or omissions or those acting on the named insured's behalf. |

| Limitations and Exclusions | Insurance for the additional insured(s) applies to the extent permitted by law, and will not exceed the scope required by any contract or agreement. Exclusions include injuries or damages occurring after the completion of work or after the work has been put to its intended use, other than by another contractor or subcontractor on the project. |

| Limits of Insurance Modification | If coverage for the additional insured(s) is mandated by a contract or agreement, the maximum payment on behalf of the additional insured is the lesser of the amount required by the contract/agreement or the available limits of insurance, without increasing the policy's overall limits. |

Filling out the CG 20 10 07 04 Liability Endorsement form is a critical step in adjusting your commercial general liability coverage to protect additional insureds as per your specific business arrangements. Following a step-by-step process can ensure that you accurately provide all the necessary information to extend these protections correctly and in compliance with any contractual obligations you have. It’s important to take your time and review all sections thoroughly to ensure that the coverage you arrange aligns with the needs of all parties involved.

Upon completing these steps, review your filled-out form to ensure all information is accurate and reflects your intentions regarding the coverage for additional insureds. It's recommended to consult with your insurance agent or legal advisor to confirm that all contractual obligations are met and that the form is fully compliant with policy requirements. Submit the endorsed form according to the instructions provided by your insurance carrier, and keep a copy for your records to document the changes made to your commercial general liability policy.

The CG 20 10 07 04 Liability Endorsement form is a document used in commercial insurance policies. It modifies the Commercial General Liability (CGL) coverage to include additional insureds—typically owners, lessees, or contractors—as protected under the policy. This extension of coverage applies to certain liabilities that arise from the acts or omissions of the policyholder or those acting on their behalf, within the scope of the policyholder’s ongoing operations for the additional insured at specified locations.

Individuals or organizations such as owners, lessees, or contractors can be added as additional insureds using this form. The specific names and operations locations must be listed in the policy’s schedule or declarations to ensure they are covered.

Coverage under this endorsement applies to liability for bodily injury, property damage, or personal and advertising injury caused, in whole or in part, by the named insured’s acts or omissions or those acting on their behalf. This liability must stem from the insured's ongoing operations conducted for the additional insured at the designated locations.

Yes, there are specific limitations:

If the coverage for additional insureds is mandated by a contract or agreement, the maximum payable amount will be either what's required by that contract/agreement or the policy’s applicable limits of insurance, depending on which is less. Importantly, adding an additional insured will not increase the overarching limits of insurance outlined in the policy.

While the CG 20 10 07 04 Endorsement extends coverage to include additional insureds for specific liabilities related to the policyholder's operations, it does not expand the overall limits of insurance. It carefully amends who is considered an insured under the policy conditions, without altering the fundamental nature of the coverage provided by the CGL policy itself.

Information necessary to add an additional insured, such as the names of persons or organizations and locations of covered operations, should be fully detailed in the policy's schedule or declarations section. It’s crucial to provide complete and accurate information to ensure the intended coverage is properly extended to additional insureds.

Filling out the CG 20 10 07 04 Liability Endorsement form requires careful attention to detail, and making errors can lead to significant consequences, including insufficient coverage or complete denial of a claim. Here are seven common mistakes people make when completing this form:

Incorrectly identifying the additional insured. One of the most frequent errors involves not properly naming the additional insured person(s) or organization(s). This mistake can occur if there is a typo, use of an incorrect legal name, or omission of vital information. It is crucial that the name(s) listed match exactly those on contracts or agreements to ensure the intended party is covered.

Omitting location(s) of covered operations. Another common error is failing to specify the location(s) of covered operations. This endorsement extends liability coverage to additional insureds specifically for operations at designated locations. If these locations are not clearly detailed, it might result in disputes about whether a particular incident is covered.

Inaccurate description of operations. Providing a vague or inaccurate description of the ongoing operations can lead to misunderstandings about the scope of coverage. The form requires specific information about the operations for which the additional insured needs coverage, thus clarity and accuracy are paramount.

Ignoring state laws and regulations. The coverage afforded to the additional insured is subject to limitations as permitted by law. Some applicants fail to consider local laws and regulations that could affect how coverage is applied, potentially resulting in unforeseen restrictions or exclusions of coverage.

Assuming broader coverage than mandated by contract. A misunderstanding or assumption that the coverage will be broader than what is required by the contract or agreement with the additional insured can lead to significant issues. It is essential to review and match the coverage limits and terms to those outlined in the contractual agreement, as the insurance provided will not exceed these requirements.

Overlooking additional exclusions. The form outlines specific exclusions for the additional insureds that applicants sometimes overlook. One of the most significant is the exclusion for bodily injury or property damage occurring after all work has been completed or put to its intended use. Not understanding these exclusions can lead to surprises in the event of a claim.

Misinterpreting the limits of insurance. Lastly, there is often confusion regarding the limits of insurance for additional insureds, especially when coverage is mandated by a contract or agreement. The form clearly states that the most it will pay on behalf of the additional insured is the lesser of the amount required by the contract or the available limits of insurance. Misinterpreting this can result in an expectation of coverage that exceeds the policy’s actual limits.

When it comes to insuring businesses, particularly in the construction or leasing sectors, the CG 20 10 07 04 Additional Insured – Owners, Lessees or Contractors – Scheduled Person or Organization Liability Endorsement form is a critical document. However, this form rarely stands alone. To fully cover the spectrum of risks and legal requirements, several other forms and documents are usually utilized alongside it. Each serves a unique purpose, contributing to the overarching goal of comprehensive coverage and compliance.

Together, these documents form a matrix of legal and financial protections, each one addressing different facets of liability and risk management. They ensure that businesses, and any additional insured entities, are adequately protected against a range of potential legal and financial liabilities. When utilized correctly, these forms help build a robust framework for managing the complex interplay of liability, operations, and contractual obligations inherent in modern business operations.

The CG 20 37 (Additional Insured – Owners, Lessees or Contractors – Automatic Status When Required in Construction Agreement With You) is a document that shares similarities with the CG 20 10 by providing additional insured status to certain parties in a construction project. Both forms are designed to extend coverage to owners, lessees, or contractors when a contract necessitates such coverage. However, the CG 20 37 automatically grants this status when a written contract requires it, without the need to individually schedule each additional insured. This broadens the insurance coverage umbrella for parties involved in construction projects, mirroring the intention behind the CG 20 10 to safeguard against risks from operations performed by or on behalf of the named insured.

The CG 20 33 (Additional Insured – Owners, Lessees or Contractors – Completed Operations) also parallels the CG 20 10, specifically in the context of offering additional insured status. While the CG 20 10 focuses on ongoing operations, the CG 20 33 extends this coverage to include completed operations. This distinction is crucial for parties requiring protection from liability or damages that occur after the named insured's work on the project is finished. Both forms address the need for extending liability coverage beyond the immediate terms of engagement, ensuring comprehensive protection against potential legal or financial liabilities.

Another related document, the CG 00 01 (Commercial General Liability Coverage Form), underpins the structure of the CG 20 10. It outlines the fundamental liability coverage that the CG 20 10 amends to include additional insureds. The CG 00 01 sets the stage by detailing the core coverage areas, exclusions, and limits of insurance, which are then modified by the CG 20 10 to accommodate the needs of additional insureds. Through this interaction, the endorsement form and the base policy work in tandem to create a customized insurance solution for commercial entities.

The CA 20 48 (Pollution Liability Broadened Coverage for Covered Autos) endorsement shares a thematic resemblance with the CG 20 10, insofar as both modify an existing policy to meet specific coverage needs. While the CG 20 10 addresses general liability issues by adding additional insureds, the CA 20 48 focuses on broadening auto liability coverage to include pollution liability events. These endorsements represent the insurance industry's flexibility in adapting base policies to cover a wide range of risk exposures through targeted adjustments.

Similarly, the CG 24 26 (Amendment of Insured Contract Definition) endorsement impacts the scope of covered activities and responsibilities under a commercial general liability policy, echoing the purpose of the CG 20 10 to modify existing coverage. By altering the definition of an "insured contract," this form can significantly influence the extent of liability protection provided, just as the CG 20 10 aims to explicitly define the coverage parameters for additional insureds. Both forms are essential tools in managing the risks associated with contractual relationships and operations.

The ISO Form CP 00 10 (Building and Personal Property Coverage Form) is involved in property insurance, yet it relates to the CG 20 10 through its role in shaping comprehensive risk management strategies. While it primarily concerns property damage and loss, the methodology of outlining coverage, exclusions, and endorsements mirrors the CG 20 10’s approach to modifying general liability coverage. Together, these forms exemplify how various types of insurance are structured to protect commercial interests comprehensively.

Filling out the CG 20 10 07 04 Liability Endorsement form requires attention to detail and an understanding of the implications of the information provided. Here are some dos and don'ts to consider:

Do:One common misconception is that the CG 20 10 07 04 form provides blanket coverage for all types of liabilities. In reality, it specifically amends the commercial general liability coverage to include additional insureds, but only in relation to liability for bodily injury, property damage, or personal and advertising injury caused by the named insured or those acting on their behalf. This means it does not cover every liability imaginable for the additional insured.

Many believe that this endorsement grants unlimited coverage to additional insureds. However, the insurance afforded to such additional insureds only applies to the extent permitted by law and will not be broader than required by a contract or agreement necessitating the additional insured status. This restriction emphasizes the need for clear contracts and understanding of legal requirements.

Another misconception is that the coverage for additional insureds extends indefinitely. The reality is that the insurance does not apply to injuries or damages occurring after all work at the location of the covered operations has been completed, or after any part of "your work" has been used by anyone other than another contractor or subcontractor. This means there is a definite boundary to the period during which the policy provides coverage.

Some assume that the CG 20 10 endorsement automatically increases the policy's limits of insurance for additional insureds. However, it clearly states that the most the insurer will pay on behalf of the additional insured is the amount required by the contract or the available limits of insurance, whichever is less, and this endorsement does not increase the overall limits of insurance.

There's a misunderstanding that this form can be used to add any party as an additional insured without specific criteria. The truth is, individuals or organizations can only be added as an additional insured with respect to liability directly linked to the named insured's acts, omissions, or ongoing operations. This requirement is crucial in ensuring relevance and legality of the additional insured status.

Finally, it is often mistakenly thought that obtaining this endorsement is an exhaustive process requiring extensive modifications to the existing policy. While it’s true that this endorsement changes the policy, the process is streamlined with basic information provided for the additional insureds and covered operations scheduled upfront. This simplification facilitates understanding and adherence to the policy's stipulations.

The CG 20 10 07 04 Liability Endorsement form serves a crucial role in modifying the scope of coverage under a Commercial General Liability (CGL) policy. It's imperative to understand the nuances of how this form operates within the framework of insurance coverage, in order to ensure that the additional insureds—generally, entities such as owners, lessees, or contractors—gain the intended protective measures against specific liabilities associated with ongoing operations. Here are key takeaways for effectively filling out and utilizing this form:

Ultimately, the successful implementation of the CG 20 10 07 04 Liability Endorsement form depends on a thorough understanding of these elements. Insurance professionals and policyholders alike must diligently ensure that all pertinent parties have the protection they need in alignment with the legal and contractual obligations at hand.

Dd Form 2870 Release of Information - The DD 2870 form is used to authorize the release of medical or dental information to a designated party.

Electrical Load Calculation - Contributes to the overall efficiency of the building process by ensuring electrical systems are correctly planned.