Fill Out Your Business Credit Application Template

Fill Out Your Business Credit Application Template

Starting a business relationship on the right foot often involves extending or obtaining credit, and this is where a Business Credit Application form becomes invaluable. It serves as a comprehensive tool that helps businesses to evaluate potential credit relationships by gathering relevant financial information and assessing the creditworthiness of the applicant. This form typically covers personal details of the applicant, business information, trade references, and the terms of credit requested. It plays a crucial role in the decision-making process, enabling creditors to make informed choices about who they lend to and under what terms. Additionally, the Business Credit Application form helps in establishing clear expectations between the parties, laying the groundwork for a transparent and accountable financial relationship. Through this form, businesses not only protect their financial interests but also build a foundation for future financial interactions by setting clear terms from the outset. It’s a step that signifies the beginning of many successful business ventures, provided it’s approached with the seriousness and diligence it warrants.

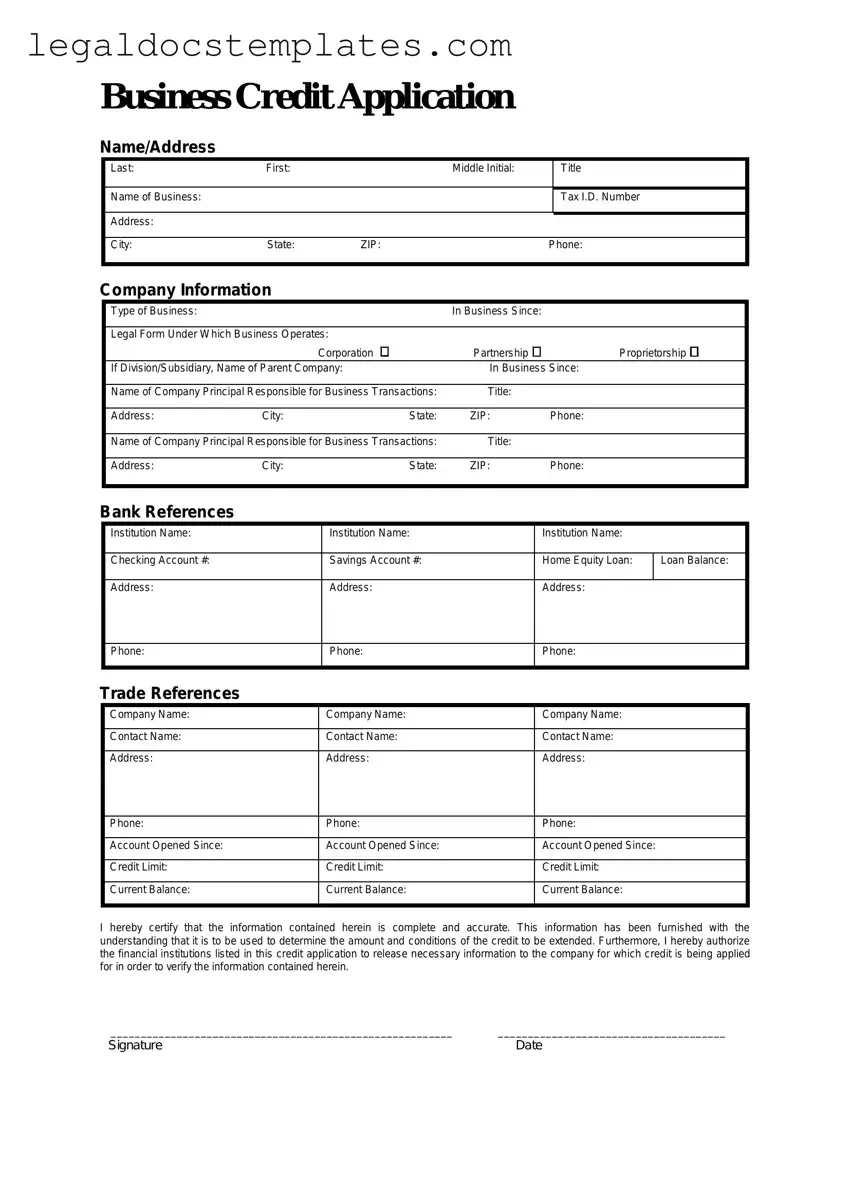

Business Credit Application

Name/Address

Last: |

First: |

|

Middle Initial: |

|

Title |

|

|

|

|

|

|

Name of Business: |

|

|

|

|

Tax I.D. Number |

|

|

|

|

|

|

Address: |

|

|

|

|

|

|

|

|

|

|

|

City: |

State: |

ZIP: |

|

Phone: |

|

|

|

|

|

|

|

Company Information

|

Type of Business: |

|

|

|

In Business Since: |

|

|

|

|

|

|

|

|

|

|

||

|

Legal Form Under Which Business Operates: |

|

|

|

|

|||

|

|

|

Corporation |

Partnership |

Proprietorship |

|

||

|

If Division/Subsidiary, Name of Parent Company: |

In Business Since: |

|

|||||

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

||

|

Name of Company Principal Responsible for Business Transactions: |

Title: |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Address: |

City: |

|

State: |

ZIP: |

Phone: |

|

|

|

|

|

|

|

|

|

|

|

Bank References |

|

|

|

|

|

|

|

|

|

Institution Name: |

|

|

Institution Name: |

|

Institution Name: |

||

|

|

|

|

|

|

|

|

|

|

Checking Account #: |

|

|

Savings Account #: |

|

Home Equity Loan: |

ILoan Balance: |

|

|

Address: |

|

|

Address: |

|

Address: |

|

|

Phone:

Phone:

Phone:

Trade References

Company Name: |

Company Name: |

Company Name: |

|

|

|

Contact Name: |

Contact Name: |

Contact Name: |

|

|

|

Address: |

Address: |

Address: |

|

|

|

Phone: |

Phone: |

Phone: |

|

|

|

Account Opened Since: |

Account Opened Since: |

Account Opened Since: |

|

|

|

Credit Limit: |

Credit Limit: |

Credit Limit: |

|

|

|

Current Balance: |

Current Balance: |

Current Balance: |

|

|

|

I hereby certify that the information contained herein is complete and accurate. This information has been furnished with the understanding that it is to be used to determine the amount and conditions of the credit to be extended. Furthermore, I hereby authorize the financial institutions listed in this credit application to release necessary information to the company for which credit is being applied for in order to verify the information contained herein.

_________________________________________________________ ______________________________________

Signature |

Date |

| Fact Name | Description |

|---|---|

| Purpose | Used by businesses to apply for credit with a lender or supplier. |

| Contents | Typically includes business information, financial statements, and credit references. |

| Governing Laws | Varies by state; usually governed by state commercial codes and federal lending regulations. |

| Processing Time | Can vary from a few days to several weeks, depending on the lender and completeness of the application. |

| Importance of Accuracy | Accurate information is crucial to avoid delays or denials of credit. |

Completing a Business Credit Application form is a crucial step in securing credit for your business, enabling expansion, inventory purchases, and managing cash flow more effectively. This document requires precise information regarding your business and its financial standing. The process, although straightforward, demands attention to detail to ensure accuracy and increase your chances of obtaining the desired credit. Below is a step-by-step guide to help you navigate this process smoothly.

After completing and submitting the Business Credit Application form, the lender will begin the evaluation process, which may include a review of your business’s credit history, financial statements, and references provided. It's important to maintain open communication and respond promptly to any additional information requests. Approval times can vary, so patience is key while waiting for a response. Once approved, you will be one step closer to achieving your business's financial goals.

A Business Credit Application form is a document used by businesses to request credit from a lender or supplier. It contains information about the business applying for credit, including details about its financial stability, credit history, and the amount of credit being requested. This form is an important step in obtaining financing or trade credit necessary for doing business.

To complete a Business Credit Application form, you will typically need the following information:

The processing time can vary significantly depending on the lender or supplier and the complexity of your application. Generally, it can take anywhere from a few days to several weeks. Prompt submission of all requested documents and information can help speed up the process.

Filling out a Business Credit Application is important because:

Yes, a Business Credit Application can be denied. Common reasons for denial include insufficient credit history, low credit scores, poor financial health of the business, or incomplete application information. Understanding these factors can help businesses improve their chances of approval in the future.

To improve your chances of getting your Business Credit Application approved, consider the following tips:

While many Business Credit Application forms contain similar types of information, there is no single standard format. Different lenders or suppliers may have their own specific forms and requirements. However, most applications will request detailed information about your business's financial situation, credit history, and the specifics of the credit request. Always check with the specific credit provider for their requirements.

Filling out a Business Credit Application form is a critical step for any company seeking to establish or expand its credit line. However, during this process, several common mistakes can significantly impact the success of the application. One primary error is the failure to provide complete information. Applicants often overlook fields or assume certain details are not significant, leaving parts of the form blank. This oversight can delay the process as the lender may need to request additional information, or it might even lead to a decline in the application due to perceived lack of transparency.

Another frequent mistake is not double-checking the application for errors. Typos, incorrect figures, and outdated information can not only affect the credibility of your business but also result in financial discrepancies that could have been avoided. It's crucial to review all entries meticulously to ensure accuracy and reliability of the data provided.

Many businesses also neglect to verify their business credit score before applying. Understanding your credit score beforehand allows you to address any potential issues that could negatively impact the lender's decision. It also helps in setting realistic expectations and possibly improving your credit score before the application, thereby increasing your chances of approval.

A common pitfall is the misunderstanding of terms and conditions, leading to the mistake of not clarifying the loan terms before submitting the application. Businesses should fully understand the interest rates, repayment terms, and any other conditions tied to the credit. Not asking questions or assuming the terms are standard can lead to unexpected financial strains in the future.

Some applicants make the error of failing to provide sufficient collateral when required. Depending on the nature of the credit and the lender's requirements, collateral might be necessary to secure the loan. Failing to offer or properly document valuable assets that can serve as collateral weakens your application and can result in denial of the credit.

Omitting relevant financial documents is another mistake. A comprehensive package of financial statements, tax returns, and other relevant documents is often necessary to accompany a Business Credit Application. When businesses fail to attach all required documentation, they inadvertently prolong the process and diminish their credibility in the eyes of the lender.

Last but not least, businesses often neglect to consider the impact of existing debts. Lenders assess a company's debt-to-income ratio to determine its repayment capacity. When existing debts are not accurately reported or considered, it can lead to an overestimation of the ability to take on new debt, thereby jeopardizing the application. Thoroughly evaluating and disclosing all existing financial obligations is crucial for a successful credit application.

By avoiding these common mistakes, businesses can improve their chances of successfully securing credit, thereby supporting their growth and financial stability.

When businesses apply for credit, the process involves more than just filling out a Business Credit Application form. To thoroughly evaluate a business's creditworthiness, lenders often require several additional documents. These documents help paint a complete picture of a business's financial health, operational history, and the legitimacy of its operations. Below is a list of documents that are frequently used alongside the Business Credit Application form, each playing a crucial role in the credit evaluation process.

Together, these documents provide a comprehensive overview of a business’s operations, financial stability, and the risk it poses to lenders. They are essential in helping lenders make informed decisions on whether to extend credit and under what terms. Ensuring that these documents are accurate and up-to-date can significantly improve a business's chances of securing credit.

The Business Credit Application form shares similarities with the Personal Credit Application form. While the former is used by businesses seeking to establish a line of credit with a supplier or financial institution, the latter serves a similar purpose for individuals. Both documents collect financial information, credit history, and references to assess the creditworthiness of the applicant. The key difference lies in the applicant's nature—one targets businesses, and the other focuses on individuals. They are alike in their fundamental purpose to secure credit under agreed-upon terms and conditions.

Another document akin to the Business Credit Application form is the Loan Application form. Used by individuals or businesses seeking to obtain a loan from a bank or other lending institutions, this form includes detailed personal or business financial information, purpose of the loan, and the collateral offered, if any. Like the Business Credit Application, it initiates a review process by the lender to determine the applicant's creditworthiness and the risk involved in extending credit or a loan. The methodologies of both documents are structured to mitigate financial risk for the lender while providing access to funds for the borrower.

The Business Plan is also somewhat comparable to the Business Credit Application form. A Business Plan outlines a company's objectives, strategies, financial forecasts, and market analysis. Though its primary function is to serve as a roadmap for the business’s growth and to attract investors, it similarly provides comprehensive financial information and projections. This information can be pivotal in persuading creditors or partners of the business’s viability and creditworthiness, akin to the objective of a Business Credit Application, albeit in a more detailed and broad-spectrum format.

The Credit Card Application form, whether intended for personal or business use, resembles the Business Credit Application form to a great extent. This form is used to apply for a credit card, requesting detailed financial information from the applicant, their credit history, and income verification, much like its business counterpart. The decision to approve or decline the credit card is based on the assessment of these details, closely mirroring the process of a Business Credit Application. Both aim to evaluate the risk of extending credit to the applicant based on their financial stability and history.

Last but not least, the Vendor Application form displays similarities to the Business Credit Application form. This document is used by businesses seeking to become suppliers or partners with other organizations. It typically requests business-related information, including financial stability, product or service offerings, and company background. While its purpose is more centered around establishing a supply chain relationship than extending a line of credit, both forms assess the reliability and financial health of the business entity. They ensure that the business dealings are conducted with financially sound and credible partners or clients.

Applying for business credit is a crucial step for the growth and sustainability of your venture. It unlocks avenues for financing that can fuel your operations, expand your business, or help manage cash flow. However, the process involves careful preparation and attention to detail. To guide you through a smoother application journey, here are five dos and don'ts when filling out a Business Credit Application form:

Dos:

Don'ts:

Remember, taking the time to meticulously prepare and review your Business Credit Application can significantly impact the outcome. A well-prepared application not only demonstrates your commitment and professionalism but also increases your chances of obtaining the desired business credit.

When it comes to securing credit for a business, the Business Credit Application form is a critical step. However, there are several misconceptions about this form that need to be clarified:

When it comes to managing the financial interactions between businesses, the Business Credit Application form plays a crucial role. It's designed to gather essential information from a business seeking credit from another business. Filling out and using this form effectively requires attention to detail and an understanding of what the information will be used for. Here are key takeaways to consider:

Understanding these key aspects can help businesses navigate the credit application process more smoothly and establish favorable credit terms that support their operational needs and financial health.

Renew My Passport Australia - Remember, the appearance of your photo in the passport will differ due to security printing techniques. It's designed for security, not photo quality.

Letter of Permission to Travel - Failure to provide a signed NCL Parental Consent form can result in the minor being excluded from participation, highlighting the form’s importance.

Check My Transcript - Lists specific deductions taken, including self-employment tax deduction and total adjustments to income.