Fill Out Your Broker Price Opinion Template

Fill Out Your Broker Price Opinion Template

In the real estate industry, a critical tool used for assessing property value is the Residential Broker Price Opinion (BPO). This document bridges the gap between an informal market assessment and a formal appraisal, providing a comprehensive look at a property's worth through the lens of current market conditions. It begins with an evaluation of the general market, considering factors such as economic climate, employment rates, and housing demand, to paint a picture of the overall market health and its direction. The form delves into specifics, such as the percentage of owner-occupied homes versus tenant-occupied homes in the neighborhood and the availability of comparable listings. The heart of the BPO lies in its thorough comparison of the subject property against others within the vicinity, meticulously documenting each one's attributes, from sale price to square footage and even the days on market. This level of detail extends to closed sales data, where recent transactions are analyzed to adjust the property's value considering various factors, including location and condition. Furthermore, it addresses the property's marketability, suggesting strategies for sale, identifying necessary repairs to enhance its appeal, and estimating the cost of these enhancements. Competitive listings are also scrutinized, offering a view of the current market offerings and how the property stacks up. Finally, the BPO culminates in a conclusion that provides an estimated market value, suggesting a listing price that reflects both the as-is condition and hypothetical repaired state, alongside a quick sale value which denotes a lower price point aimed at accelerating the sale process. Authenticated by the signature of the sales representative, the Broker Price Opinion form serves as a pivotal instrument in real estate transactions, guiding decisions for lenders, investors, and homeowners alike.

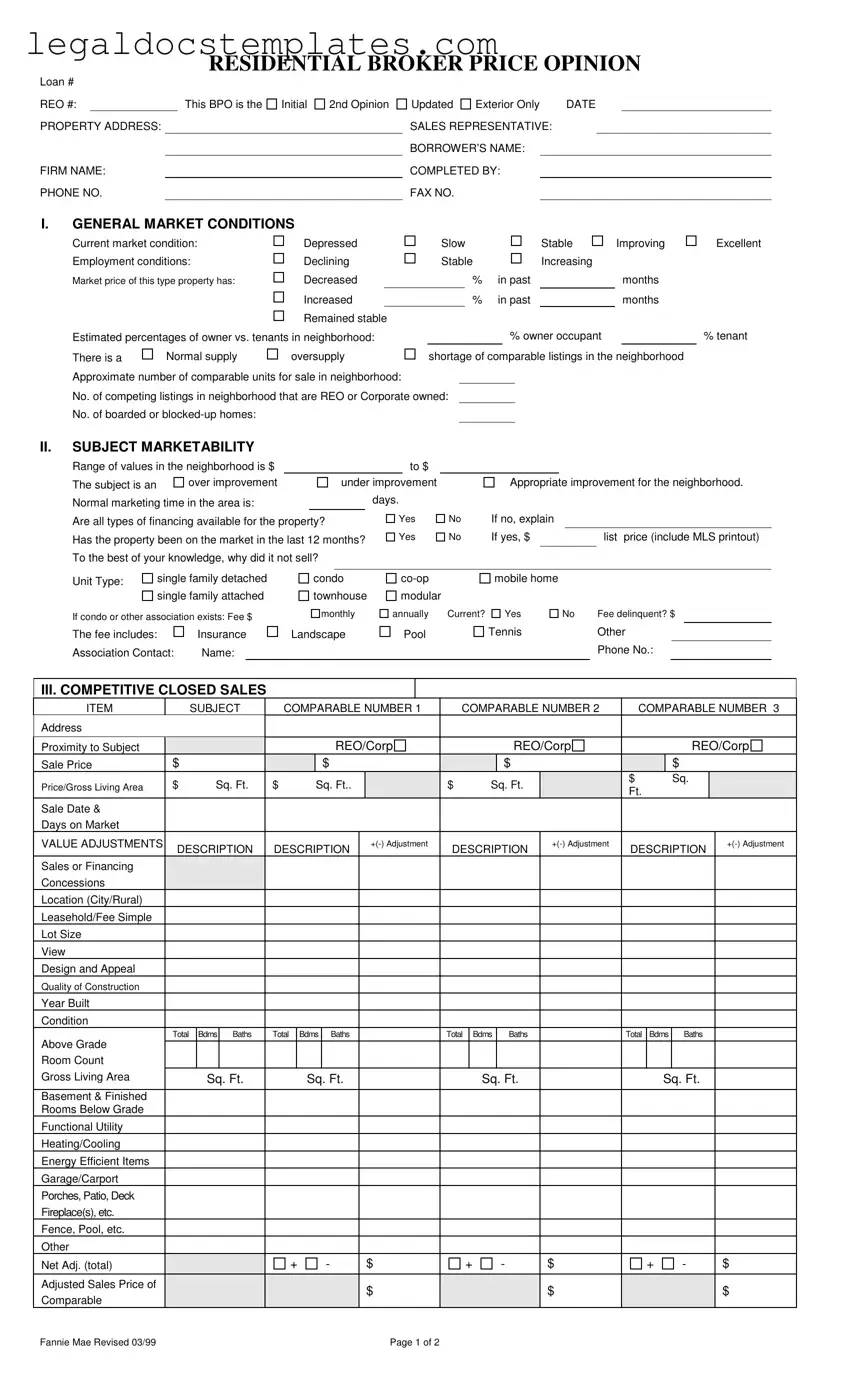

RESIDENTIAL BROKER PRICE OPINION

Loan #

REO #:This BPO is the

PROPERTY ADDRESS:

FIRM NAME:

PHONE NO.

Initial

2nd Opinion

Updated Exterior Only |

DATE |

|||

SALES REPRESENTATIVE: |

|

|

|

|

BORROWER’S NAME: |

|

|

|

|

COMPLETED BY: |

|

|

|

|

FAX NO. |

|

|

|

|

I.GENERAL MARKET CONDITIONS

Current market condition: |

Depressed |

Slow |

|

Stable |

Improving |

||

Employment conditions: |

Declining |

Stable |

|

Increasing |

|

||

Market price of this type property has: |

Decreased |

|

|

% |

in past |

|

months |

|

Increased |

|

|

% |

in past |

|

months |

|

Remained stable |

|

|

|

|

|

|

Estimated percentages of owner vs. tenants in neighborhood: |

|

|

% owner occupant |

|

|||

There is a |

Normal supply |

oversupply |

shortage of comparable listings in the neighborhood |

||||

Approximate number of comparable units for sale in neighborhood: |

|

|

|

|

|

||

No. of competing listings in neighborhood that are REO or Corporate owned:

No. of boarded or

Excellent

% tenant

II.SUBJECT MARKETABILITY

Range of values in the neighborhood is $ |

|

|

|

|

|

to $ |

|

|

|

|

|

|

|

|

The subject is an |

over improvement |

|

|

under improvement |

|

Appropriate improvement for the neighborhood. |

||||||||

Normal marketing time in the area is: |

|

|

|

|

days. |

|

|

|

|

|

|

|||

Are all types of financing available for the property? |

Yes |

No |

If no, explain |

|

|

|

||||||||

Has the property been on the market in the last 12 months? |

Yes |

No |

If yes, $ |

|

|

list price (include MLS printout) |

||||||||

To the best of your knowledge, why did it not sell? |

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||||

Unit Type: |

single family detached |

|

condo |

|

mobile home |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

single family attached |

|

townhouse |

modular |

|

|

|

|

|

|

||||

If condo or other association exists: Fee $

monthly

annually Current?

Yes

No |

Fee delinquent? $ |

The fee includes:

Association Contact:

Insurance

Name:

Landscape

Pool

Tennis |

Other |

|

Phone No.: |

III. COMPETITIVE CLOSED SALES

ITEM |

|

|

SUBJECT |

|

COMPARABLE NUMBER 1 |

|

COMPARABLE NUMBER 2 |

|

COMPARABLE NUMBER 3 |

|||||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

||||||||

Sale Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|||

Price/Gross Living Area |

$ |

|

Sq. Ft. |

$ |

|

Sq. Ft.. |

|

|

$ |

|

|

Sq. Ft. |

|

|

$ |

|

|

|

Sq. |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

Ft. |

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Sale Date & |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

|

DESCRIPTION |

|

|

DESCRIPTION |

|

DESCRIPTION |

|

||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

Bdms |

Baths |

|

Total |

Bdms |

|

Baths |

|

|

|

Total |

|

Bdms |

|

Baths |

|

|

Total |

Bdms |

Baths |

|

|

|

||||||

Above Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

Sq. Ft. |

|

|

Sq. Ft. |

|

|

|

|

|

|

Sq. Ft. |

|

|

|

|

|

Sq. Ft. |

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Adj. (total) |

|

|

|

|

|

+ |

- |

|

|

$ |

|

+ |

- |

|

$ |

|

+ |

|

|

- |

|

$ |

|

|||||||||

Adjusted Sales Price of |

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

$ |

|

Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fannie Mae Revised 03/99 |

|

|

|

|

|

|

|

|

|

|

|

|

Page 1 of 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REO# |

Loan # |

IV. MARKETING STRATEGY

Minimal Lender Required Repairs |

V. REPAIRS

Occupancy Status: Occupied

Repaired Most Likely Buyer:

Vacant

Unknown

Unknown

Owner occupant

Investor

Investor

Itemize ALL repairs needed to bring property from its present “as is” condition to average marketable condition for the neighborhood. Check those repairs you recommend that we perform for most successful marketing of the property.

$

$

$

$

$

$

$

$

$

$

|

|

|

|

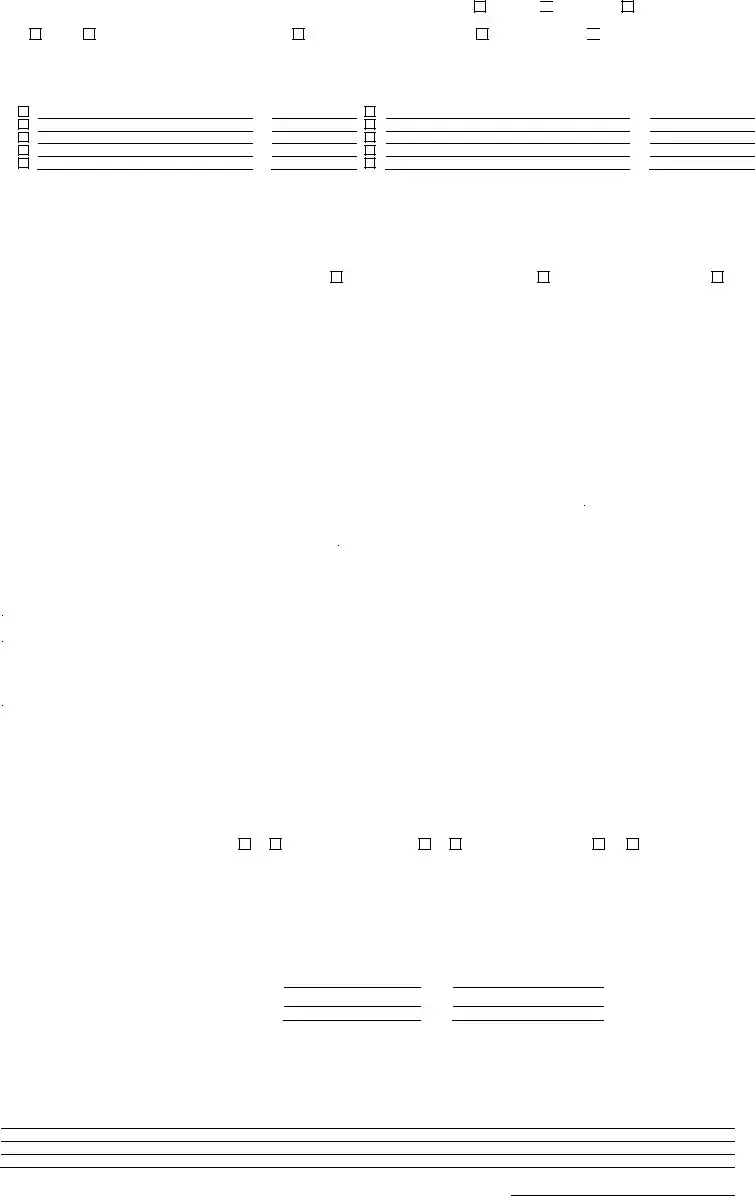

GRAND TOTAL FOR ALL REPAIRS $ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. COMPETITIVE LISTINGS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

ITEM |

|

|

SUBJECT |

COMPARABLE NUMBER 1 |

COMPARABLE NUMBER. 2 |

COMPARABLE NUMBER. 3 |

|||||||||||||||||||||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proximity to Subject |

|

|

|

|

|

REO/Corp |

|

|

|

|

|

REO/Corp |

|

|

REO/Corp |

||||||||||||

List Price |

$ |

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

||

Price/Gross Living Area |

$ |

|

Sq.Ft. |

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

|

$ |

Sq.Ft. |

|

|

||||||||||

Data and/or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Verification Sources |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VALUE ADJUSTMENTS |

|

DESCRIPTION |

DESCRIPTION |

|

+ |

DESCRIPTION |

|

DESCRIPTION |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales or Financing |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Concessions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Days on Market and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date on Market |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Location (City/Rural) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Leasehold/Fee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Simple |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lot Size |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

View |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Design and Appeal |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Quality of Construction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Built |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Condition |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Above Grade |

Total |

Bdms |

Baths |

Total |

Bdms |

Baths |

|

|

|

Total |

Bdms |

|

Baths |

|

Total |

Bdms |

|

Baths |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Room Count |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Living Area |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

Sq. Ft. |

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

|

Sq. Ft. |

|

|

|||||||||||||

Basement & Finished |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Rooms Below Grade |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Functional Utility |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Heating/Cooling |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Energy Efficient Items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Garage/Carport |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Porches, Patio, Deck |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fireplace(s), etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fence, Pool, etc. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Net Adj. (total) |

|

|

|

|

+ |

- |

|

|

|

$ |

|

|

+ |

- |

- |

|

$ |

|

|

+ |

- |

|

$ |

|

|

||

Adjusted Sales Price |

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

of Comparable |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

VI. THE MARKET VALUE (The value must fall within the indicated value of the Competitive Closed Sales).

Market Value |

Suggested List Price |

AS IS REPAIRED

30 Quick Sale Value

Last Sale of Subject, Price |

Date |

COMMENTS (Include specific positives/negatives, special concerns, encroachments, easements, water rights, environmental concerns, flood zones, etc. Attach addendum if additional space is needed.)

Signature: |

|

Date: |

Fannie Mae Revised 03/99 |

Page 2 of 2 |

CMS Publishing Company 1 800 |

| Fact | Detail |

|---|---|

| 1. Purpose | This BPO form is used to provide an estimated price for a residential property. |

| 2. Types of BPO | Includes Initial, 2nd Opinion, Updated, and Exterior Only opinions. |

| 3. Market Conditions Assessment | Evaluates the current market and employment conditions, supply of listings, and percentage of owner-occupied homes. |

| 4. Subject Marketability | Assesses the property's marketability, including financing availability and prior market exposure. |

| 5. Competitive Sales Analysis | Compares subject property with up to 3 comparable sales to adjust market value. |

| 6. Marketing Strategy | Suggests marketing strategies, including as-is, minimal, and lender-required repairs. |

| 7. Repairs | Lists recommended repairs to make the property marketable, with a focus on the most impactful. |

| 8. Competitive Listings Analysis | Compares subject property with up to 3 competitive listings to adjust list price. |

| 9. Market Value Estimation | Suggests AS IS, REPAIRED, and Quick Sale values based on competitive market analysis. |

Filling out a Broker Price Opinion (BPO) form is a detailed process that requires careful attention to various aspects of the property and its surrounding market. These steps will guide you in providing an accurate and comprehensive analysis of the property's value. This form plays a significant role in real estate transactions, helping lenders, investors, and others understand the property's market value. Following these steps accurately ensures a thorough evaluation, impacting key financial decisions.

Completing the Broker Price Opinion form accurately is vital for providing a reliable valuation that stakeholders can use in their decision-making. It requires a comprehensive understanding of the property, the local market, and how various factors influence property value. Following each step diligently ensures the BPO serves its purpose effectively.

A Broker Price Opinion (BPO) is an analysis conducted by a real estate broker to determine the potential selling price of a property. It is based on the examination of various factors including market conditions, property condition, and comparisons with similar properties in the area. This report is often used by financial institutions to estimate value when a full appraisal is not necessary.

BPOs are commonly used in situations such as loan originations, refinancing, or for estimating the value of a property in a short sale or foreclosure. They offer a cost-effective alternative to a full property appraisal and are usually faster to complete.

A typical BPO contains:

While both BPOs and appraisals aim to determine the value of a property, they differ in complexity, cost, and who performs them. An appraisal is a more detailed evaluation conducted by a licensed appraiser. It is usually more costly and time-consuming than a BPO, which is less comprehensive and performed by a real estate broker or agent.

Yes, BPOs come in two main types:

BPOs are usually requested by lenders, mortgage companies, and investment firms, often in the context of loan originations, foreclosures, refinancing, or portfolio management. Homeowners considering a short sale might also request one to understand the potential listing price of their property.

The accuracy of a BPO can vary based on the broker’s experience, the property’s condition, and market dynamics. Although not as detailed as an appraisal, BPOs can be quite precise when conducted by knowledgeable and experienced brokers.

Yes, homeowners can request a BPO if they want an estimate of their home’s value. This can be useful for planning a sale, understanding home equity, or in discussions with banks for loan modifications.

The cost of a BPO is typically lower than a full property appraisal. Charges can vary depending on the property’s location, size, and the type of BPO required (interior vs. exterior). It’s best to consult with a broker for specific pricing.

The timeframe for completing a BPO can vary, but most are completed within a few days to a week after the broker’s inspection of the property. The exact time will depend on the availability of comparable market data and the speed of the broker’s investigation.

Filling out the Broker Price Opinion (BPO) form correctly is crucial for accurate real estate valuations, yet mistakes are common. One common error occurs in the assessment of general market conditions. Professionals sometimes inaccurately describe the current market due to a lack of comprehensive research or recent developments they may not be aware of. Describing the market as "stable" when it is actually "improving" or vice versa can lead to significant discrepancies in valuation. Such inaccuracies not only mislead lenders but also affect decision-making processes related to the property in question.

Another area frequently mishandled is the subject marketability section. Here, incorrect evaluations regarding the appropriateness of improvements or the normal marketing time can be observed. For instance, considering an improvement 'appropriate' for the neighborhood without a detailed assessment of the local trends or failing to account for the increasing demand which might reduce the normal marketing time, skew the property's perceived value. These errors can ultimately guide a property to be undervalued or overvalued in the market.

A third significant oversight is in the section pertaining to competitive closed sales. Often, incorrect adjustments are made for differences between the subject property and comparables, such as location, size, or condition. Failing to accurately adjust these variables can drastically alter the property's estimated value. For instance, overlooking the impact of a recent sale of a similar property in the immediate vicinity, or misjudging the value adjustment for a property's superior condition, can result in an erroneous final valuation.

Last but not least, inaccuracies in the repair section can also lead to incorrect valuations. Underestimating or overestimating the cost of repairs needed to bring the property to an average marketable condition for the neighborhood is a common mistake. Recommending unnecessary repairs or neglecting needed ones affects the suggested as-is and repaired values, potentially misleading investors or financial institutions about the true cost of making the property market-ready. This can result in financial decisions based on flawed assumptions about the property's condition and value.

When engaging in real estate transactions, especially in evaluating a property's worth, the Broker Price Opinion (BPO) form is a critical document. However, to ensure a holistic assessment and a seamless transaction process, multiple other forms and documents accompany the BPO. These documents not only provide a comprehensive understanding of the property's value but also ensure legal compliance and facilitate informed decision-making. Here are six additional forms and documents often paired with the BPO form:

The synergy of the Broker Price Opinion form with these adjunct documents ensures a transparent, accurate, and effective property valuation process. For individuals or entities involved in real estate transactions, understanding the significance and utility of each document is paramount for successful negotiations and compliance with legal requirements. Each document plays a vital role in painting a comprehensive picture of the property’s value, condition, and legal standing, streamlining the transaction process and safeguarding the interests of all involved parties.

The Comparative Market Analysis (CMA) shares significant similarities with the Broker Price Opinion (BPO) form. Both documents provide an estimate of a home's market value, often used by real estate professionals to help sellers set listing prices or to inform buyers on offering prices. Like the BPO, a CMA lists comparable sales, market conditions, and adjustments for different features or conditions of the subject property versus the comparables. The main goal of both documents is to offer an accurate market value estimation based on current market trends and comparable sales data.

Appraisal reports, while more formal and detailed than BPOs, serve a parallel purpose of determining a property's value. Appraisals are typically required by lenders before loan approvals to ensure the property's market value meets or exceeds the loan amount. They include thorough inspections and often more detailed adjustments compared to BPOs, considering aspects of the property and market conditions to come to a finalized value. Appraisers are usually licensed professionals whose reports carry significant weight in financing decisions.

The Home Inspection Report, although distinct in its primary purpose from a BPO, shares the commonality of providing detailed information on the condition of a property. While a BPO assesses market value with a focus on sales and market data, home inspections concentrate on the physical state of the property, reporting on the condition of the home's systems, structure, and any repairs needed. However, both can influence the sale or purchase of a home by highlighting areas that may require attention before a transaction can be completed successfully.

Listing Agreements contain details that can be found in a BPO, such as the property's projected selling price and current market analysis, albeit for a different purpose. These contracts between sellers and real estate agents outline the terms under which a property will be marketed, including the list price which often relies on data similar to what's found in a BPO. The intersection between these documents lies in their use of market data to inform decisions related to selling properties.

The Purchase Agreement, while primarily a legal document formalizing the agreement between buyer and seller regarding the terms of a sale, often relies on information found in a BPO. The agreed-upon sale price can be influenced by the BPO's determination of property value, making these documents indirectly connected. As negotiations progress, the value indicated by the BPO can serve as a basis for discussions on final sale price and terms.

Real Estate Owned (REO) Property Reports are closely related to BPOs in the context of foreclosed properties owned by lenders. These reports assess the value of REO properties to aid in pricing for resale, taking into account factors like condition, market comparables, and repair needs, much like a BPO. The goal is to sell the property efficiently and for a price reflective of its market value, making both documents integral to the process of handling REO listings.

Lastly, the Property Condition Report, similar to sections of the BPO, offers an overview of the physical state and needed repairs for a property. While it does not directly assess market value, it impacts the valuation process by detailing repair costs and issues that may affect the property’s sale price. Understanding the property's condition is crucial for accurate pricing strategies, making this report complementary to the valuation objectives of a BPO.

When you're tasked with filling out a Broker Price Opinion (BPO) Form, precision and attention to detail are paramount. This document plays a critical role in the real estate industry, providing valuable insights into property values. Below are some essential dos and don'ts to help guide you through the process.

Things you should do:

Verify all the property details meticulously. Ensuring accuracy in the basics like the address, firm name, and contact information sets the right foundation.

Assess current market conditions with care. Analyze the local market trends, including employment conditions and inventory levels, to provide an informed opinion.

Provide a thorough analysis of the subject’s marketability. Accurately describe the property's condition, taking note of any improvements or deficiencies.

Evaluate competitive market analyses (CMAs) accurately. Comparing the subject property against similar properties that have recently sold or are on the market is crucial.

Be honest when describing the property's condition and its comparison with neighborhood properties. Objective evaluation helps in forming a credible opinion.

Things you shouldn't do:

Don't rush through the form. Filling out the BPO requires careful evaluation of numerous factors. Rushing can lead to oversights and inaccuracies.

Avoid using outdated or irrelevant comparables. Always ensure that the chosen comparables reflect the current market conditions.

Don't ignore local market nuances. Whether it's a specific type of property being more desirable in the area or certain trends affecting home values, this information is vital.

Avoid subjective opinions without evidence. While your expertise is valuable, making assertions about property values should always be backed up with data and comparisons.

Attention to these dos and don’ts will not only make your BPO more accurate but also more valuable to those relying on your expertise. Remember, a well-prepared BPO can significantly influence financial and investment decisions related to real estate.

Many people have misconceptions about the Broker Price Opinion (BPO) form, which can lead to confusion about its purpose and how it is used in the real estate industry. Let's clear up some of these misunderstandings:

Understanding these misconceptions can help buyers, sellers, and real estate professionals navigate the complexities of real estate transactions with more clarity and confidence.

U.S. Corporation Income Tax Return - The IRS provides instructions for Form 1120, guiding corporations through each part of the form to ensure correct completion.

Bathroom Sheet - Strengthens farm sanitation policies by ensuring regular assessments and maintenance actions are documented.

California Odometer Disclosure Statement Pdf - A notarized form that locks in the true mileage of a vehicle for records.